U.S. SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

[X] QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the quarterly period ended June 30, 2015

[ ] TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from _________ to _________

Commission File No. 000-53078

Bone Biologics Corporation

(Exact name of registrant as specified in its charter)

| Delaware | 42-1743430 | |

| (State

or other jurisdiction of incorporation or formation) |

(I.R.S.

employer identification number) |

| 175 May Street, Suite 400, Edison, NJ, 08837 | ||

| (Address of principal executive offices and Zip Code) | ||

| (732) 661-2224 | ||

| (Registrant’s telephone number, including area code) |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Exchange Act during the preceding 12 months (or for such shorter period that the issuer was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

[X] Yes [ ] No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (Section 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

[X] Yes [ ] No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in rule 12b-2 of the Exchange Act.

| Large accelerated filer | [ ] | Accelerated filer | [ ] |

| Non-accelerated filer | [ ] | Smaller reporting company | [X] |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

[ ] Yes [X] No

As of August 14, 2015, there were 30,973,482 shares of the issuer’s common stock, $0.001 par value, outstanding.

TABLE OF CONTENTS

| 2 |

NOTE ON FORWARD-LOOKING STATEMENTS

This Quarterly Report on Form 10-Q (this “Form 10-Q”) contains forward-looking statements. Such forward-looking statements include those that express plans, anticipation, intent, contingency, goals, targets or future development and/or otherwise are not statements of historical fact. These forward-looking statements are based on our current expectations and projections about future events and they are subject to risks and uncertainties known and unknown that could cause actual results and developments to differ materially from those expressed or implied in such statements. These forward-looking statements are subject to a number of risks, uncertainties and assumptions. For a more detailed listing of some of the risks and uncertainties facing the Company, please see our Current Report on Form 10-K for the fiscal year ended December 31, 2014, filed with the Securities and Exchange Commission (“SEC”) on March 31, 2015.

All statements other than historical facts contained in this report, including statements regarding our future financial position, capital expenditures, cash flows, business strategy and plans and objectives of management for future operations are forward-looking statements. The words “anticipated,” “believe,” “expect,” “plan,” “intend,” “seek,” “estimate,” “project,” “could,” “may,” and similar expressions are intended to identify forward-looking statements. These statements include, among others, information regarding future operations, future capital expenditures, and future net cash flow. Such statements reflect our management’s current views with respect to future events and financial performance and involve risks and uncertainties, including, without limitation, our ability to raise additional capital to fund our operations, obtaining Food and Drug Administration (“FDA”) and other regulatory authorization to market our drug and biological products, successful completion of our clinical trials, our ability to achieve regulatory authorization to market our lead product Nell-1, our reliance on third party manufacturers for our drug products, market acceptance of our products, our dependence on licenses for certain of our products, our reliance on the expected growth in demand for our products, exposure to product liability and defect claims, development of a public trading market for our securities, and various other matters, many of which are beyond our control.

Should one or more of these risks or uncertainties occur, or should underlying assumptions prove to be incorrect, actual results may vary materially and adversely from those anticipated, believed, estimated or otherwise indicated. Consequently, all of the forward-looking statements made in this Form 10-Q are qualified by these cautionary statements and accordingly there can be no assurances made with respect to the actual results or developments. We undertake no obligation to revise or publicly release the results of any revision to these forward-looking statements, except as required by law. Given these risks and uncertainties, readers are cautioned not to place undue reliance on such forward-looking statements.

Unless expressly indicated or the context requires otherwise, the terms “Company,” “we,” “us,” and “our” in this document refer to Bone Biologics Corporation, a Delaware corporation, and, its wholly owned subsidiary as defined under the heading “Management’s Discussion and Analysis”in this Form 10-Q.

| 3 |

PART I – FINANCIAL INFORMATION

Bone Biologics Corporation

Condensed Consolidated Balance Sheets

| June 30, 2015 | December 31, 2014 | |||||||

| (unaudited) | ||||||||

| Assets | ||||||||

| Current assets | ||||||||

| Cash | $ | 3,166,562 | $ | 2,661,396 | ||||

| Prepaid expenses | 88,767 | 89,517 | ||||||

| Deferred financing fees | 996,947 | 983,857 | ||||||

| Other receivables – related party | 150,000 | 75,000 | ||||||

| Total current assets | 4,402,276 | 3,809,770 | ||||||

| Property and equipment, net | 10,983 | 11,621 | ||||||

| Total assets | $ | 4,413,259 | $ | 3,821,391 | ||||

| Liabilities and Stockholders’ Deficit | ||||||||

| Current liabilities | ||||||||

| Accounts payable and accrued expenses | $ | 43,141 | $ | 215,389 | ||||

| Note payable to related party | - | 3,659,328 | ||||||

| Total current liabilities | 43,141 | 3,874,717 | ||||||

| Note payable, net of debt discount | 5,268,311 | 3,645,194 | ||||||

| Total liabilities | 5,311,452 | 7,519,911 | ||||||

| Commitments and Contingencies | ||||||||

| Stockholders’ deficit | ||||||||

| Preferred Stock, $0.001 par value per share; 20,000,000 shares authorized; none issued or outstanding at June 30, 2015 and December 31, 2014 | - | - | ||||||

| Common stock, $0.001 par value per share; 100,000,000 shares authorized; 29,239,156 and 24,269,047 shares issued and outstanding at June 30, 2015 and December 31, 2014, respectively | 29,239 | 24,269 | ||||||

| Additional paid-in capital | 13,643,107 | 8,315,128 | ||||||

| Accumulated deficit | (14,570,539 | ) | (12,037,917 | ) | ||||

| Total stockholders’ deficit | (898,193 | ) | (3,698,520 | ) | ||||

| Total liabilities and stockholders’ deficit | $ | 4,413,259 | $ | 3,821,391 | ||||

See accompanying notes to unaudited condensed consolidated financial statements.

| F-1 |

Bone Biologics Corporation

Condensed Consolidated Statements of Operations

| Three Months Ended June 30, 2015 |

Three Months Ended June 30, 2014 |

Six

Months Ended June 30, 2015 |

Six Months Ended June 30, 2014 |

|||||||||||||

| (unaudited) | (unaudited) | (unaudited) | (unaudited) | |||||||||||||

| Revenues | $ | - | $ | - | $ | - | $ | - | ||||||||

| Cost of revenues | - | - | - | - | ||||||||||||

| Gross profit | - | - | - | - | ||||||||||||

| Operating expenses | ||||||||||||||||

| Research and development | 175,010 | 133,457 | 362,579 | 183,111 | ||||||||||||

| General and administrative | 335,568 | 183,037 | 1,071,419 | 307,148 | ||||||||||||

| Total operating expenses | 510,578 | 316,494 | 1,433,998 | 490,259 | ||||||||||||

| Loss from operations | (510,578 | ) | (316,494 | ) | (1,433,998 | ) | (490,259 | ) | ||||||||

| Other expenses | ||||||||||||||||

| Other expense | - | (8,140 | ) | - | (9,623 | ) | ||||||||||

| Interest expense, net | (380,225 | ) | (102,935 | ) | (1,097,024 | ) | (250,533 | ) | ||||||||

| Total other expenses | (380,225 | ) | (111,075 | ) | (1,097,024 | ) | (260,156 | ) | ||||||||

| Loss before provision for income taxes | (890,803 | ) | (427,569 | ) | (2,531,022 | ) | (750,415 | ) | ||||||||

| Provision for income taxes | - | - | 1,600 | 800 | ||||||||||||

| Net loss | $ | (890,803 | ) | $ | (427,569 | ) | $ | (2,532,622 | ) | $ | (751,215 | ) | ||||

| Weighted average shares outstanding – basic and diluted | 27,436,809 | 10,928,099 | 25,861,679 | 10,928,099 | ||||||||||||

| Loss per share – basic and diluted | $ | (0.03 | ) | $ | (0.04 | ) | $ | (0.10 | ) | $ | (0.07 | ) | ||||

See accompanying notes to unaudited condensed consolidated financial statements.

| F-2 |

Bone Biologics Corporation

Condensed Consolidated Statements of Cash Flows

| For

the Six Months Ended June 30, 2015 |

For the Six Months Ended June 30, 2014 |

|||||||

| (unaudited) | (unaudited) | |||||||

| Operating activities | ||||||||

| Net loss | $ | (2,532,622 | ) | $ | (751,215 | ) | ||

| Adjustments to reconcile net loss to net cash provided by (used in) operating activities: | ||||||||

| Depreciation | 1,142 | - | ||||||

| Accrued interest expense | 105,669 | 162,493 | ||||||

| Amortization of deferred financing costs | 537,944 | - | ||||||

| Debt discount amortization | 275,317 | 91,111 | ||||||

| Stock-based compensation | 137,412 | - | ||||||

| Warrants issued to consultants | 324,532 | - | ||||||

| Loss on sale of marketable securities | - | 9,623 | ||||||

| Changes in operating assets and liabilities: | ||||||||

| Prepaid expenses and other current assets | (74,250 | ) | 1,767 | |||||

| Deferred financing costs | (185,000 | ) | - | |||||

| Advances due to related party | - | 89,374 | ||||||

| Accounts payable and accrued expenses | (84,474 | ) | 108,095 | |||||

| Net cash (used in) operating activities | (1,494,330 | ) | (288,752 | ) | ||||

| Investing activities | ||||||||

| Purchase of property and equipment | (504 | ) | - | |||||

| Proceeds from sale of marketable securities | - | 37,377 | ||||||

| Net cash (used in) provided by investing activities | (504 | ) | 37,377 | |||||

| Financing activities | ||||||||

| Proceeds from issuance of notes payable | 2,000,000 | 250,000 | ||||||

| Net cash provided by financing activities | 2,000,000 | 250,000 | ||||||

| Net increase (decrease) in cash | 505,166 | (1,375 | ) | |||||

| Cash, beginning of period | 2,661,396 | 1,538 | ||||||

| Cash, end of period | $ | 3,166,562 | $ | 163 | ||||

| Supplemental non-cash information | ||||||||

| Issuance of warrants in connection with Notes Payable, net of amortization included above | $ | - | $ | 104,798 | ||||

| Debt and accrued interest converted into Common Shares | $ | 3,852,771 | $ | - | ||||

| Issuance of warrants in payment of financing fees | $ | - | $ | 8,180 | ||||

| Note payable received in the form of investments | $ | - | $ | 50,000 | ||||

| Interest paid | $ | 240,767 | $ | - | ||||

| Taxes paid | $ | 1,600 | $ | 800 | ||||

See accompanying notes to unaudited condensed consolidated financial statements.

| F-3 |

Bone Biologics Corporation

Notes to Unaudited Condensed Consolidated Financial Statements

1. The Company

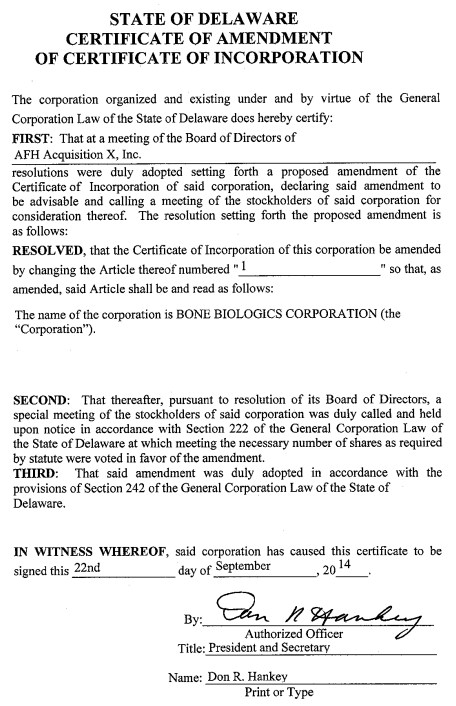

Bone Biologics Corporation (the “Company”) was incorporated under the laws of the State of Delaware on October 18, 2007 as AFH Acquisition X, Inc. Pursuant to a Merger Agreement, dated September 19, 2014, by and among the Company, its wholly-owned subsidiary, Bone Biologics Acquisition Corp., a Delaware corporation (“Merger Sub”), and Bone Biologics, Inc. Merger Sub merged with and into Bone Biologics Inc., with Bone Biologics remaining as the surviving corporation in the Merger. Upon the consummation of the Merger, the separate existence of Merger Sub ceased. On September 22, 2014 the Company officially changed its name to “Bone Biologics Corporation” (“Bone” or “Bone Biologics”) to more accurately reflect the nature of its business and Bone Biologics, Inc. became a wholly-owned subsidiary of the Company. Bone Biologics, Inc. was incorporated in California on March 9, 2004.

Bone is a biotechnology company that is currently focused on bone regeneration in spinal fusion using the recombinant human protein, known as UCB-1 (or “Nell-1”). The Nell-1 protein is an osteoinductive recombinant protein that provides target specific control over bone regeneration. The protein has been licensed exclusively for worldwide applications to Bone Biologics through a technology transfer from the University of California, Los Angeles (“UCLA”). Bone Biologics received guidance from the United States Food and Drug Administration (“FDA”) that Nell-1 will be classified as a combination product with a device lead.

The Company is a development stage entity. The production and marketing of the Company’s products and its ongoing research and development activities will be subject to extensive regulation by numerous governmental authorities in the United States. Prior to marketing in the United States, any drug developed by the Company must undergo rigorous preclinical (animal) and clinical (human) testing and an extensive regulatory approval process implemented by the FDA under the Food, Drug and Cosmetic Act. The Company has limited experience in conducting and managing the preclinical and clinical testing necessary to obtain regulatory approval. There can be no assurance that the Company will not encounter problems in clinical trials that will cause the Company or the FDA to delay or suspend clinical trials.

The Company’s success will depend in part on its ability to obtain patents and product license rights, maintain trade secrets, and operate without infringing on the proprietary rights of others, both in the United States and other countries. There can be no assurance that patents issued to or licensed by the Company will not be challenged, invalidated, or circumvented, or that the rights granted thereunder will provide proprietary protection or competitive advantages to the Company.

Recapitalization

In connection with the Merger, the 5,000,000 outstanding shares of common stock of the Company, par value $0.001 per share (“Common Stock”), prior to the Merger were consolidated into 3,853,600 shares of Common Stock and the remaining shares were cancelled.

Additionally, all of the issued and outstanding shares of Bone Biologics Inc.’s $0.0001 par value common stock converted into a combined total of 19,897,587 shares of the Company’s Common Stock (including 2,151,926 shares issuable upon the exercise of outstanding warrants and 5,648,658 shares issuable upon the conversion of debt). In exchange, Bone Biologics agreed to pay AFH Holding & Advisory, LLC (“AFH”) the principal sum of $590,000.

Going Concern and Liquidity

The Company has no significant operating history and, from March 9, 2004 (inception) to June 30, 2015, has generated a net loss of approximately $14.5 million. The Company will continue to incur significant expenses for development activities for their lead product Nell-1. Operating expenditures for the next twelve months are estimated at $5.6 million. The accompanying condensed consolidated financial statements for the six months ended June 30, 2015 have been prepared assuming the Company will continue as a going concern. In connection with the LOI (See Note 5), management intends to raise additional debt and/or equity financing to fund future operations and to provide additional working capital. However, there is no assurance that such financing will be consummated or obtained in sufficient amounts necessary to meet the Company’s needs.

| F-4 |

Bone Biologics Corporation

Notes to Unaudited Condensed Consolidated Financial Statements

The accompanying consolidated financial statements do not include any adjustments to reflect the possible future effects on the recoverability and classification of assets or the amounts and classifications of liabilities that may result from the possible inability of the Company to continue as a going concern.

2. Summary of Significant Accounting Policies

The unaudited interim condensed consolidated financial statements have been prepared by us pursuant to the rules and regulations of the Securities and Exchange Commission. The information furnished herein reflects all adjustments (consisting of normal recurring accruals and adjustments) which are, in the opinion of management, necessary to fairly present the operating results for the respective periods. Certain information and footnote disclosures normally present in the annual consolidated financial statements prepared in accordance with accounting principles generally accepted in the United States of America have been omitted pursuant to such rules and regulations. These consolidated financial statements should be read in conjunction with the audited consolidated financial statements and notes for the year ended December 31, 2014. The results of the three and six month periods ended June 30, 2015 are not necessarily indicative of the results to be expected for the full year ending December 31, 2015.

Basis of Presentation

The accompanying condensed consolidated financial statements and related notes included activities of the Company and have been prepared in conformity with accounting principles generally accepted in the United States of America (“GAAP”).

Use of Estimates

The preparation of the accompanying condensed consolidated financial statements in conformity with GAAP requires management to make certain estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the consolidated financial statements and reported amounts of expenses during the reporting period. Significant estimates include warrants and income tax valuation allowances. Actual results could differ from those estimates.

Fair Value of Financial Instruments

The Company’s consolidated financial instruments are accounts payable and notes payable. The recorded values of accounts payable approximate their values based on their short term nature. Notes payable are recorded at their issue value or if warrants are attached at their issue value less the value of the warrant.

The Company defines fair value as the exchange price that would be received for an asset or paid to transfer a liability (an exit price) in the principal or most advantageous market for the asset or liability in an orderly transaction between market participants on the measurement date. Valuation techniques used to measure fair value must maximize the use of observable inputs and minimize the use of unobservable inputs. The fair value hierarchy is based on three levels of inputs that may be used to measure fair value, of which the first two are considered observable and the last is considered unobservable:

Level 1: Quoted prices in active markets for identical assets or liabilities.

Level 2: Inputs other than Level 1 that are observable, either directly or indirectly, such as quoted prices for similar assets or liabilities; quoted prices in markets that are not active; or other inputs that are observable or can be corroborated by observable market data for substantially the full term of the assets or liabilities.

Level 3 assumptions: Unobservable inputs that are supported by little or no market activity and that are significant to the fair value of the assets or liabilities including liabilities resulting from embedded derivatives associated with certain warrants to purchase common stock.

| F-5 |

Bone Biologics Corporation

Notes to Unaudited Condensed Consolidated Financial Statements

Property and Equipment

Property and equipment are stated at cost. Depreciation is calculated using the straight-line method over the estimated useful lives of the related assets, ranging from three to seven years. Expenditures for additions and improvements are capitalized, while repairs and maintenance costs are expensed as incurred. The cost and related accumulated depreciation of property and equipment sold or otherwise disposed of are removed from the accounts and any gain or loss is recorded in the year of disposal.

Impairment of Long-Lived Assets

The long-lived assets held and used by the Company are reviewed for impairment no less frequently than annually or whenever events or changes in circumstances indicate that the carrying amount of an asset may not be recoverable. In the event that facts and circumstances indicate that the cost of any long-lived assets may be impaired, an evaluation of recoverability is performed. Management has determined that there was no impairment in the value of long-lived assets during the six months ended June 30, 2015.

Research and Development Costs

Research and development costs include, but are not limited to, patents and license expenses, payroll and other personnel expenses, consultants, expenses incurred under agreements with contract research and manufacturing organizations and animal clinical investigative sites and the cost to manufacture clinical trial materials. Costs related to research, design and development of products are charged to research and development expense as incurred.

Patents and Licenses

In March 2006, the Company entered into an exclusive license agreement (“Exclusive License Agreement”), with UCLA for the worldwide application of the Nell-1 protein through a technology transfer. See Note 5 for commitments related to the Exclusive License Agreement. Patent expenses include costs to acquire the license of Nell -1, which was de minimus, and costs to file patent applications related to Nell-1.

The Company expenses the costs incurred to file patent applications, all costs related to abandoned patent applications and maintenance costs, and these costs are included in research and development expenses. Costs associated with licenses acquired to be able to use products from third parties prior to receipt of regulatory approval to market the related products are also expensed. The Company’s licensed technologies may have alternative future uses in that they are enabling (or platform) technologies that can be the basis for multiple products that would each target a specific indication. Costs of acquisition of licenses are expensed.

Deferred Financing Costs

Deferred financing costs represent costs incurred in connection with the issuance of the convertible notes payable and private equity financing. Deferred financing costs related to the issuance of debt are being amortized over the term of the financing instrument using the effective interest method, while deferred financing costs from equity financings are netted against the gross proceeds received from the equity financings.

As a result, the deferred financing cost as of December 31, 2014 was $983,857. During the six months period ended June 30, 2015, the Company incurred and capitalized $187,530 related cost due to the May 2015 financing. As of June 30, 2015, the deferred financing cost was $996,947. Amortization of deferred financing costs was $174,440 and $-0- for the six months ended June 30, 2015 and 2014, respectively.

| F-6 |

Bone Biologics Corporation

Notes to Unaudited Condensed Consolidated Financial Statements

Other receivables – related party

Other receivables – related party represent a receivable from AFH, a shareholder, for fees paid on their behalf for legal services. There are no established repayment terms. During the six months ended June 30, 2015 the Company paid a retainer of $75,000 to AFH for contemplated advisory services.

Concentration of Credit Risk and Other Risks and Uncertainties

Cash balances are maintained at financial institutions and, at times, balances may exceed federally insured limits. The Company has never experienced any losses related to these balances. As of January 1, 2013, federal insurance coverage is $250,000 per depositor at each financial institution. A substantial majority of the Company’s cash balances exceed federally insured limits.

Stock Based Compensation

ASC 718, Compensation – Stock Compensation, prescribes accounting and reporting standards for all share-based payment transactions in which employee services are acquired. Transactions include incurring liabilities, or issuing or offering to issue shares, options, and other equity instruments such as employee stock ownership plans and stock appreciation rights. Share-based payments to employees, including grants of employee stock options, are recognized as compensation expense in the consolidated financial statements based on their fair values. That expense is recognized over the period during which an employee is required to provide services in exchange for the award, known as the requisite service period (usually the vesting period).

The Company accounts for stock-based compensation issued to non-employees and consultants in accordance with the provisions of ASC 505-50, Equity – based Payments to Non-Employees. Measurement of share-based payment transactions with non-employees is based on the fair value of whichever is more reliably measurable: (a) the goods or services received; or (b) the equity instruments issued. The fair value of the share-based payment transaction is determined at the earlier of performance commitment date or performance completion date.

Income Taxes

Income taxes are provided for the tax effects of transactions reported in the consolidated financial statements and consist of taxes currently due and deferred taxes resulting from timing differences in recording of transactions for tax purposes and financial reporting purposes.

The deferred tax assets and liabilities represent the future tax return consequences of those differences, which will either be taxable or deductible when the assets and liabilities are received or settled. Valuation allowances are established when necessary to reduce deferred tax assets to amounts expected to be realized.

The accounting provisions related to uncertain income tax positions require the Company to determine whether any tax position in all open years meets a more likely than not threshold of being sustained upon examination by the applicable taxing authority. The Company did not have any changes to its liability for uncertain tax positions as at June 30, 2015 and December 31, 2014.

The Company’s policy is to recognize interest and/or penalties related to income tax matters in income tax expense. No such amounts are accrued as of June 30, 2015 and December 31, 2014.

| F-7 |

Bone Biologics Corporation

Notes to Unaudited Condensed Consolidated Financial Statements

Loss per Common Share

The Company utilizes FASB ASC Topic No. 260, Earnings per Share. Basic loss per share is computed by dividing loss available to common shareholders by the weighted-average number of common shares outstanding. Diluted loss per share is computed similar to basic loss per share except that the denominator is increased to include the number of additional common shares that would have been outstanding if the potential common shares had been issued and if the additional common shares were dilutive. Diluted loss per common share reflects the potential dilution that could occur if convertible debentures, options and warrants were to be exercised or converted or otherwise resulted in the issuance of common stock that then shared in the earnings of the entity.

Since the effects of outstanding options, warrants, and the conversion of convertible debt are anti-dilutive in all periods presented, shares of common stock underlying these instruments have been excluded from the computation of loss per common share.

The following sets forth the number of shares of common stock underlying outstanding options, warrants, and convertible debt as of June 30, 2015 and 2014:

| June 30, | ||||||||

| 2015 | 2014 | |||||||

| Warrants | 9,621,235 | 634,300 | ||||||

| Stock options | 757,977 | - | ||||||

| Convertible promissory notes | 4,430,380 | 5,520,528 | ||||||

| 14,809,592 | 6,154,828 | |||||||

New Accounting Standards

The Company has reviewed all recently issued, but not yet adopted, accounting standards in order to determine their effects, if any, on its results of operation, financial position or cash flows. Based on that review, the Company believes that none of these pronouncements will have a significant effect on its condensed consolidated financial statements.

| F-8 |

Bone Biologics Corporation

Notes to Unaudited Condensed Consolidated Financial Statements

In June 2014, the FASB issued ASU 2014-12, “Compensation - Stock Compensation (Topic 718), Accounting for Share-Based Payments When the Terms of an Award Provide That a Performance Target Could be Achieved after the Requisite Service Period.” This ASU provides more explicit guidance for treating share-based payment awards that require a specific performance target that affects vesting and that could be achieved after the requisite service period as a performance condition. The new guidance is effective for annual and interim reporting periods beginning after December 15, 2015. The Company does not expect the adoption of this guidance to have a material impact on the consolidated financial statements.

In August 2014, the FASB issued ASU 2014-15, “Presentation of Financial Statements – Going Concern (Topic 205-40),” which requires management to evaluate whether there is substantial doubt about an entity’s ability to continue as a going concern for each annual and interim reporting period. If substantial doubt exists, additional disclosure is required. This new standard will be effective for the Company for annual and interim periods beginning after December 15, 2016. Early adoption is permitted. The Company adopted this new standard for the fiscal year ending December 31, 2014.

In April 2015, the FASB issued ASU 2015-3, “Interest - Imputation of Interest (Subtopic 835-30),” related to the presentation of debt issuance costs. This standard will require debt issuance costs related to a recognized debt liability to be presented on the balance sheet as a direct deduction from the debt liability rather than as an asset. These costs will continue to be amortized to interest expense using the effective interest method. This pronouncement is effective for fiscal years, and for interim periods within those fiscal years, beginning after December 15, 2015, and retrospective adoption is required. We will adopt this pronouncement for our year beginning January 1, 2016. We do not expect this pronouncement to have a material effect on our consolidated financial statements.

3. Property and Equipment

Property and equipment consist of the following at:

| June 30, 2015 | December 31, 2014 | |||||||

| Furniture and equipment | $ | 12,405 | $ | 11,901 | ||||

| Less accumulated depreciation | (1,422 | ) | (280 | ) | ||||

| $ | 10,983 | $ | 11,621 | |||||

Depreciation expense for the six months ended June 30, 2015 and 2014 was $1,142 and $-0-, respectively.

4. Accounts Payable and Accrued Expenses

Accounts payable and accrued expenses consist of the following:

| June 30, 2015 | December 31, 2014 | |||||||

| Interest expense | $ | - | $ | 87,774 | ||||

| Accounts payable | 32,440 | 119,776 | ||||||

| Payroll liabilities | 10,701 | 7,839 | ||||||

| $ | 43,141 | $ | 215,389 | |||||

| F-9 |

Bone Biologics Corporation

Notes to Unaudited Condensed Consolidated Financial Statements

5. Commitments and Contingencies

Letter of Intent

In August of 2012, Bone Biologics, Inc., along with its then majority owner and debt holder, Musculoskeletal Transplant Foundation (“MTF”), entered into a Letter of Intent (“LOI”) with AFH to consummate a business combination through a share exchange, reverse merger, or other similar transactions resulting in the Company becoming a public entity (the “Transaction”). In August 2013, the LOI was amended and restated, and on May 7, 2014, the LOI was again amended and restated. The Amended and Restated Letter of Intent dated May 7, 2014 (the “Amended LOI”) contemplates and defines the following events:

Consummation of Bridge Financings (“Closing I”)

In April 2013 and September 2013, the Company’s Board approved the Company to borrow up to an aggregate principal amount of $300,000 (the “April Bridge Financing”) and $250,000 (the “September Bridge Financing”) pursuant to the sale and issuance of convertible promissory notes and warrants to purchase common stock of the Company (collectively, the “Bridge Financings”). The note accrues interest at a rate of 12% per year and is payable each quarter. A warrant to purchase the Company’s common stock equal to 50% of the original principal amount at $1.00 per share was issued to each Bridge Financing participant. Principal and unpaid accrued interest may be converted into equity securities issued in the Company’s next equity financing in an aggregate amount of at least $2.5 million at a price equal to the price paid by investors in the next equity financing. On April 29, 2013 and on June 5, 2013, the Company borrowed $100,000 from MTF and $100,000 from Orthofix, Corp. (“Orthofix”), respectively, under the April Bridge Financing. In September 2013, the Company borrowed $50,000 from AFH under the April Bridge Financing. In October 2013, the Company borrowed an additional $150,000 from Orthofix under the September Bridge Financing.

Consummation of Business Combination (“Closing II”)

Under the Amended LOI, it was contemplated that the Company and its equity holders would consummate a share exchange, reverse merger, or other business combination with a Delaware corporation publicly reporting pursuant to United States Securities Exchange Act of 1934, as amended (the “Exchange Act”), or a private Delaware corporation (“Acquisition Co.”), either directly or indirectly through an affiliate. If the post-business combination entity was not already a corporation publicly reporting pursuant to the Exchange Act, AFH would assist the post-business combination entity with the filing of an appropriate registration statement resulting in the Company becoming a public company (“PubCo”). The Company affected a merger on September 19, 2014 (See Note 1 Recapitalization). AFH received $590,000 in connection with the business combination.

| F-10 |

Bone Biologics Corporation

Notes to Unaudited Condensed Consolidated Financial Statements

Consummation of the Private Placement (“Closing III”)

Subsequent to Closing II, AFH agreed to use its best efforts to assist PubCo in procuring one or more investors for a private financing, whether debt or equity, of up to $10.0 million. Such transaction is to include an over-allotment option of 15% at AFH’s discretion (the “Private Placement”). At the consummation of Closing III, AFH received warrants to purchase up to 500,000 share of common stock of PubCo at the per share price of the shares offered in the Private Placement with a 5 year term and a cashless exercise provision (the “Extra Warrants”).

Consummation of the PIPE Transaction (“Closing IV”)

Subsequent to Closing III, AFH will use its best efforts to assist PubCo in procuring an investment bank (the “Bank”) to facilitate a private investment in public equity transaction in an amount between $8.0 million and $10.0 million through the sale of securities of PubCo (the “PIPE”). Such transaction will include a 15% over allotment at AFH and/or the Bank’s discretion. Such transaction is contingent upon the appointment of a Bank and filing appropriate forms with the Financial Industry Regulatory Authority (“FINRA”).

Consummation of Initial Public Offering (“Closing V”)

Subsequent to Closing IV, AFH will assist PubCo in procuring a Bank to act as underwriter for an initial public offering in an amount of up to $40.0 million (the “Initial Public Offering”). The Initial Public Offering shall include a 15% over allotment option at AFH and/or the Bank’s discretion. Such a transaction is contingent upon the appointment of the Bank.

License Commitment

In connection with the Exclusive License Agreement, the Company is required to pay a royalty fee beginning in the first year of commercial sale of the licensed product equal to 3% of net sales on a quarterly basis with an annual minimum royalty of $25,000 for the life of the patent rights. In addition to the royalty fees, the Company is also required to pay UCLA a $10,000 annual maintenance fee, $50,000 upon FDA marketing approval and $25,000 upon first commercial sale.

On October 22, 2013, the Exclusive License Agreement was amended. The following additional fees will be due to UCLA: i) 2% of the amount raised in the Private Placement or, if the Private Placement did not close or was less than $2.5 million then a fee of $100,000 was due and payable by June 1, 2014, ii) $25,000 due upon closing of Phase 1 clinical trial and iii) $50,000 due upon closing of Phase 3 clinical trial. The Company paid the fee of $100,000 in June 2014. Furthermore, the Agreement was modified in that we shall pay the Regents $25,000 for closing of Phase 1 clinical trial and $50,000 for closing of Phase 3 clinical trial. This amendment also stipulates that human clinical trials will commence no later than December 31, 2015. Management believes they will not commence human clinical trials before the expiration of our current license. While the Company will continue to use commercially reasonable efforts to achieve this milestone, the parties are engaged in discussions to amend the license agreement but there are no assurances that an agreement can be reached.

Contingencies

The Company is subject to claims and assessments from time to time in the ordinary course of business. The Company’s management does not believe that any such matters, individually or in the aggregate, will have a material adverse effect on the Company’s business, financial condition, results of operations or cash flows.

Indemnification

In the normal course of business, the Company enters into contracts and agreements that contain a variety of representations and warranties and provide for general indemnifications. The Company’s exposure under these agreements is unknown because it involves claims that may be made against the Company in the future, but have not yet been made. To date, the Company has not paid any claims or been required to defend any action related to its indemnification obligations. However, the Company may record charges in the future as a result of these indemnification obligations.

| F-11 |

Bone Biologics Corporation

Notes to Unaudited Condensed Consolidated Financial Statements

In accordance with its amended and restated certificate of incorporation and amended and restated bylaws, the Company has indemnification obligations to its officers and directors for certain events or occurrences, subject to certain limits, while they are serving at the Company’s request in such capacity. There have been no claims to date and the Company has a director and officer insurance policy that enables it to recover a portion of any amounts paid for future potential claims.

6. Notes Payable to Related Party

As of June 30, 2015 and December 31, 2014, the Company’s notes outstanding, with MTF a related party, consisted of the following:

| Note Type | Issue Date | Maturity Date | Interest Rate | June 30, 2015 | December 31, 2014 | |||||||||||||||

| New MTF Convertible Promissory Note | 9/19/14 | 3/31/15 | 8.5 | % | -0- | 3,747,102 | ||||||||||||||

| Less: Accrued interest expense | -0- | 87,774 | ||||||||||||||||||

| Notes payable to related party | $ | -0- | $ | 3,659,328 | ||||||||||||||||

Convertible Related Party Promissory Notes

The related party convertible promissory notes are considered hybrid instruments, which consist of a debt host instrument together with a conversion feature, thus giving the holder of a convertible note an option to convert into an equity instrument providing the holder a residual interest in the Company. The holder of a convertible promissory note also has the option to present its convertible promissory note to the Company and demand payment under the terms of the note after the maturity date or upon the occurrence of certain events such as the failure of the Company to make a payment on the note when due, bankruptcy or certain other liquidation events. The Company concluded that the convertible promissory note would be accounted for as a typical debt instrument with related interest expense recorded in the Company’s statements of operations. The Company concluded that there is no beneficial conversion feature as of the date of issuance of the convertible notes. However, the note contains a contingent feature whereby the conversion rate may be lowered if a financing occurs at a lower rate than the note’s conversion rate. If the contingency is met and the conversion feature is determined to be “beneficial” in a future accounting period, an additional financing cost would be recorded for the beneficial conversion feature in the Company’s statements of operations at that time.

New MTF Convertible Note

On September 19, 2014, MTF’s 2008 and 2009 Promissory Notes and any related loan agreements, credit agreements, guarantee agreements or other agreements related to the MTF 2008 and 2009 Promissory Notes were cancelled and the Company issued MTF a convertible promissory note in the face amount of $3,659,328 (the “New MTF Convertible Note”). Pursuant to the terms of the New MTF Convertible Note, 50% of all principal and accrued and unpaid interest due under the New MTF Convertible Note will be converted into common stock of the Company upon the closing of the PIPE. The remainder of the New MTF Convertible Note, including all accrued and unpaid interest, will be converted upon consummation of the Initial Public Offering.

On May 4, 2015, MTF converted their New MTF Convertible Note in the amount of $3,659,328 plus accrued interest of $193,443 into 2,438,463 shares of Common Stock of the Company.

| F-12 |

Bone Biologics Corporation

Notes to Unaudited Condensed Consolidated Financial Statements

7. Notes Payable

Convertible Notes Payable

The convertible promissory notes are considered hybrid instruments, which consist of a debt host instrument together with a conversion feature, thus giving the holder of a convertible note an option to convert into an equity instrument providing the holder a residual interest in the Company. The holder of a convertible promissory note also has the option to present its convertible promissory note to the Company and demand payment under the terms of the note after the maturity date or upon the occurrence of certain events such as the failure of the Company to make a payment on the note when due, bankruptcy or certain other liquidation events. The Company concluded that the convertible promissory notes would be accounted for as a typical debt instrument with related interest expense recorded in the Company’s statements of operations. The Company concluded that there is no beneficial conversion feature as of the date of issuance of the convertible notes.

Secured Convertible Note and Warrant

On October 24, 2014, the Company issued a convertible promissory note in the amount of $5,000,000 (the “Convertible Note”) to Hankey Capital, LLC (“Hankey Capital”). The Convertible Note matures on October 24, 2017 (the “Maturity Date”) and bears interest at an annual rate of interest of the “prime rate” (as quoted in the “Money Rates” section of The Wall Street Journal) plus 4.0%, with a minimum rate of 8.5% per annum until maturity, with interest payable monthly in arrears. Prior to the Maturity Date, Hankey Capital has a right, in their sole discretion, to convert the Convertible Note into shares of the Company’s Common Stock, at a conversion rate equal to the greater of (i) $1.58 per share and (ii) 70% of the average daily price for the Common Stock as measured over the course of the 60 day period prior to the conversion.

The Convertible Note is secured by certain collateral shares of Common Stock issued by the Company in the name of Hankey Capital, in such amount so as to maintain a loan to value ratio of no greater than 50% (the “Collateral”). 6,329,114 shares were issued upon closing the Convertible Note. The number of shares in the Collateral shall be adjusted on a yearly basis. The shares representing the Collateral contain a restrictive legend. The Company shall seek to register the Collateral shares initially delivered on the date of the Convertible Note pursuant to a registration rights agreement (the “Registration Rights Agreement”) as described below. Upon the effectiveness of such Registration Statement, the Company will remove the restrictive legends from the Collateral shares so long as Hankey Capital agrees in any event not to sell any Collateral shares if Hankey Capital is notified that the Registration Statement is no longer effective. Hankey Capital may hold the Collateral in any brokerage account of its choosing, but shall not transfer, sell or otherwise dispose of any Collateral, except during the existence of an Event of Default, as defined in the Convertible Note. The Convertible Note is further secured by collateral assignments of all the Company’s license agreements.

The principal amount of the loan is pre-payable in whole or in part at any time, without premium or penalty. Upon any voluntary partial prepayment of outstanding principal, Hankey Capital shall return Collateral shares to the Company in the amount necessary, if any, to maintain the loan to value ratio at no less than 50%. Upon a full payment of the outstanding principal, all Collateral shares shall be returned return and cancelled. Hankey Capital shall also return Collateral shares under the same terms in case of partial or full conversion of the Convertible Note.

The Company paid a commitment fee in the amount of $150,000 (3% of the original principal amount of the loan) to Hankey Capital. The Company intends to use the proceeds of the Convertible Note for working capital and general corporate purposes.

On October 24, 2014, the Company also issued a warrant to Hankey Capital for 3,955,697 shares of Common Stock at an exercise price per share of $1.58 (the “Warrant”). The Warrant will expire on October 24, 2017. The Warrant also includes such other terms that are normal and customary for warrants of this type.

| F-13 |

Bone Biologics Corporation

Notes to Unaudited Condensed Consolidated Financial Statements

Registration Rights Agreement

On October 24, 2014, the Company entered into a Registration Rights Agreement with Hankey Capital, for certain demand registration rights and unlimited piggyback registration rights for the shares underlying the Convertible Note and the Warrant, and subject to an agreed lock up period. Pursuant to the Registration Rights Agreement, Hankey Capital may at any time request registration of their registrable shares. Within 30 days of such demand, the Company will provide written notice of such request to all other holders of registrable securities and will include in such registration all registrable shares with respect to which the Company has received written requests for inclusion within twenty-five (25) days after delivery of the Company’s notice. The Company has agreed to pay all registration expenses relating to up to three long-form registrations or short-form registrations for Hankey Capital.

Whenever the Company proposes to register any of its securities under the Securities Act of 1933, as amended (the “Securities Act”)(other than pursuant to a demand registration under the Registration Rights Agreement) and the registration form to be used may be used for the registration of any registrable shares, the Company will give prompt written notice to all holders of the registrable shares of its intention to effect such a registration and will include in such registration all registrable shares (in accordance with the priorities set forth in the Registration Rights Agreement) with respect to which the Company has received written requests for inclusion within fifteen (15) days after the delivery of the Company’s notice. Pursuant to Registration Rights Agreement, holders of registrable shares and the Company agree not to effect any public sale or distribution of equity securities of the Company, or any securities convertible into or exchangeable or exercisable for such securities, during the six (6) months following, the effective date of the Company’s merger with Bone Biologics, Inc. on September 19, 2014.

On October 24, 2014, Forefront Capital (“Forefront”) was issued a warrant to purchase 126,582 shares of Common Stock upon completion of the Hankey Capital Convertible Note.

2nd Secured Convertible Note and Warrant

On May 4, 2015, the Company issued a convertible promissory note in the amount of $2,000,000 (the “2nd Convertible Note”) to Hankey Capital. The 2nd Convertible Note matures on May 4, 2018 (the “2nd Maturity Date”) and bears interest at an annual rate of interest of the “prime rate” (as quoted in the “Money Rates” section of The Wall Street Journal) plus 4.0%, with a minimum rate of 8.5% per annum until maturity, with interest payable monthly in arrears. Prior to the 2nd Maturity Date, Hankey Capital has a right, in their sole discretion, to convert the 2nd Convertible Note into shares of the Company’s Common Stock, at a conversion rate equal to the greater of (i) $1.58 per share or (ii) 70% of the average daily price for the Common Stock as measured over the course of the 60 day period prior to the conversion.

The 2nd Convertible Note is secured by certain collateral shares of Common Stock issued by the Company in the name of Hankey Capital, in such amount so as to maintain a loan to value ratio of no greater than 50% (the “2nd Collateral”). The number of shares in the 2nd Collateral shall be adjusted on a yearly basis. The shares representing the 2nd Collateral contain a restrictive legend. Hankey Capital may hold the 2nd Collateral in any brokerage account of its choosing, but shall not transfer, sell or otherwise dispose of any 2nd Collateral, except during the existence of an Event of Default, as defined in the 2nd Convertible Note. The 2nd Convertible Note is further secured by collateral assignments of all the Company’s license agreements.

The principal amount of the loan is pre-payable in whole or in part at any time, without premium or penalty. Upon any voluntary partial prepayment of outstanding principal, Hankey Capital shall return 2nd Collateral shares to the Company in the amount necessary, if any, to maintain the loan to value ratio at no less than 50%. Upon a full payment of the outstanding principal, all the collateral shares shall be returned return and cancelled. Hankey Capital shall also return the collateral shares under the same terms in case of partial or full conversion of the 2nd Convertible Note.

| F-14 |

Bone Biologics Corporation

Notes to Unaudited Condensed Consolidated Financial Statements

In connection with the 2nd Convertible Note to Hankey Capital, on May 4, 2015 the Company issued 2,531,646 common shares as collateral.

The Company paid a commitment fee in the amount of $60,000 (3% of the original principal amount of the loan) to Hankey Capital. The Company intends to use the proceeds of the Convertible Note for working capital and general corporate purposes.

On May 4, 2015, the Company also issued a warrant to Hankey Capital for 1,898,734 shares of Common Stock at an exercise price per share of $1.58 (the “2nd Warrant”). The 2nd Warrant will expire on May 4, 2018. The 2nd Warrant includes such other terms that are normal and customary for warrants of this type.

Under the terms of both the 2nd Convertible Note and the 2nd Warrant, at any time that any of the Company’s equity securities are registered under Section 12 of the Securities and Exchange Act of 1934, the aggregate number of Common Stock shares that may be acquired by Hankey Capital upon any exercise of any conversion under the 2nd Convertible Note or exercise of the 2nd Warrant, shall be limited to the extent necessary to insure that, following such exercise, or other acquisition, the total number of Common Stock shares then beneficially owned by Hankey Capital and its affiliates may not exceed 4.999% of the total number of issued and outstanding Common Stock. The Company shall, instead of issuing or transferring Common Stock in excess of this limitation, suspend its obligation to issue Common Stock in excess of the foregoing limitation until such time, if any, as such Common Stock shares may be issued in compliance with such limitation; provided, that, by written notice to the Company, Hankey Capital may waive the provisions of this section or increase or decrease the maximum percentage to any other percentage specified in such notice; provided further that any such waiver or increase or decrease will not be effective until the 61st day after such notice is received by the Company.

The total debt discount costs related to our outstanding debt for the six months ended June 30, 2015 and 2014, was $275,317 and $91,111, respectively. These costs were amortized to interest expense. The unamortized debt discount at June 30, 2015 was $1,731,689. The cost is expected to be recognized over a period of 2.5 years. The unamortized debt discount at December 31, 2014 was $1,354,806.

| Note Type | Issue Date | Maturity Date | Interest Rate | June 30, 2015 | December 31, 2014 | |||||||||||||||

| Secured Convertible Note | 10/24/14 | 10/24/17 | 8.5 | % | 5,000,000 | 5,000,000 | ||||||||||||||

| 2nd Secured Convertible Note | 5/4/15 | 5/4/18 | 8.5 | % | 2,000,000 | -0- | ||||||||||||||

| Less: Debt discount | 1,731,689 | 1,354,806 | ||||||||||||||||||

| Net Notes payable | $ | 5,268,311 | $ | 3,645,194 | ||||||||||||||||

8. Stockholders’ Equity

Preferred Stock

The Company’s amended and restated certificate of incorporation authorizes the Company to issue a total of 20,000,000 shares of preferred stock. No shares have been issued.

Common Stock

The Company’s amended and restated certificate of incorporation authorizes the Company to issue a total of 100,000,000 shares of common stock. As of June 30, 2015 and December 31, 2014, the Company had an aggregate of 29,239,156 shares and 24,269,047 shares of common stock outstanding, respectively.

In connection with the Secured Convertible Notes to Hankey Capital, the Company issued 8,860,760 common shares as collateral. (See Note 7)

Each share of common stock has the right to one vote. The holders of common stock are also entitled to receive dividends whenever funds are legally available and when declared by the Board of Directors, subject to the prior rights of holders of all classes of stock outstanding having priority rights as to dividends. No dividends have been declared by the Board.

| F-15 |

Bone Biologics Corporation

Notes to Unaudited Condensed Consolidated Financial Statements

Common Stock Warrants

As of June 30, 2015, the Company had outstanding unexercised Common Stock Warrants as follows:

| Date Issued | Exercise Price | Number of Shares | Expiration date | ||||||||

| 2006 | $ | 0.17 | 60,920 | October 31, 2016 | |||||||

| 2009 | $ | 0.44 | 118,383 | March 16, 2019 | |||||||

| 2010 | $ | 0.44 | 254,997 | February 4 , 2020 | |||||||

| April 2013 | $ | 1.00 | 50,000 | April 28, 2020 | |||||||

| June 2013 | $ | 1.00 | 50,000 | June 4, 2020 | |||||||

| September 2013 | $ | 1.00 | 25,000 | September 20, 2020 | |||||||

| November 2013 | $ | 1.00 | 75,000 | November 14, 2020 | |||||||

| July 2014 | $ | 1.50 | 166,667 | May 30, 2018 | |||||||

| July 2014 | $ | 1.50 | 166,667 | June 30, 2018 | |||||||

| July 2014 | $ | 1.00 | 500,000 | June 30, 2018 | |||||||

| July 2014 | $ | 1.00 | 46,667 | July 2, 2018 | |||||||

| July 2014 | $ | 0.00 | 12,625 | July 10, 2018 | |||||||

| September 2014 | $ | 1.62 | 625,000 | August 31, 2021 | |||||||

| September 2014 | $ | 1.00 | 699,671 | September 18, 2021 | |||||||

| September 2014 | $ | 1.00 | 89,588 | September 29, 2021 | |||||||

| October 2014 | $ | 1.00 | 126,582 | October 23, 2017 | |||||||

| October 2014 | $ | 1.58 | 3,955,697 | October 23, 2017 | |||||||

| February 2015 | $ | 1.58 | 699,037 | February 14, 2018 | |||||||

| May 2015 | $ | 1.58 | 1,898,734 | May 4, 2018 | |||||||

| Total warrants at June 30, 2015 | 9,621,235 | 3.32 years | |||||||||

Agent Warrants

Our engagement with Forefront expired without renewal on February 15, 2015. Under the agreement, Forefront or its designees received the following warrant (“Agency Warrant”). Such Agent Warrant was issued at the closing of the Private Placement and provided, among other things, that the Agent Warrant shall: (i) be exercisable at the price of the securities (or the exercise price of the securities) issued to the investors in the offering, (ii) expire five (5) years from the date of issuance, (iii) include customary registration rights, including the registration rights provided to the Investors, (iv) contain provisions for cashless exercise and (v) include such other terms that are normal and customary for warrants of this type. In addition, Forefront or its designees received an additional warrant (“Advisory Warrant”) equal to 2.0% of the Company’s post-merger and financing fully diluted shares outstanding upon the closing of $2.5 million of investors on which Forefront is eligible to receive compensation.

On February 15, 2015, Forefront was issued the Advisory Warrant to purchase 699,037 shares of Common Stock which represents 2.0% of the Company’s post-merger fully diluted shares outstanding at $1.58 per share upon expiration of their engagement. The warrants expire in three years from issuance date. The initial fair value of the warrants was estimated at an aggregate value of $363,499, using the Black-Scholes option pricing model with the following assumptions at the date of issuance: expected volatility of 97.76%, risk-free interest rate of 1.10%, contractual term of 3 years and dividend yield of 0%.

No common stock warrants were exercised or expired during the six months period June 30, 2015 and 2014.

9. Stock-based Compensation

2014 Stock Option Plan

2,642,898 shares of our Common Stock have been initially authorized and reserved for issuance under our 2014 Stock Option Plan as option awards. This reserve may be increased by the Board on January 1, 2015 and each subsequent anniversary through January 1, 2024 by up to the number of shares of stock equal to 5% of the number of shares of stock issued and outstanding on the immediately preceding December 31. Appropriate adjustments will be made in the number of authorized shares and other numerical limits in our 2014 Stock Option Plan and in outstanding awards to prevent dilution or enlargement of participants’ rights in the event of a stock split or other change in our capital structure. Shares subject to awards granted under our 2014 Stock Option Plan which expire, are repurchased or are cancelled or forfeited will again become available for issuance under our 2014 Stock Option Plan. The shares available will not be reduced by awards settled in cash. Shares withheld to satisfy tax withholding obligations will not again become available for grant. The gross number of shares issued upon the exercise of stock appreciation rights or options exercised by means of a net exercise or by tender of previously owned shares will be deducted from the shares available under our 2014 Stock Option Plan.

Awards may be granted under our 2014 Stock Option Plan to our employees, including officers, director or consultants, and our present or future affiliated entities. While we may grant incentive stock options only to employees, we may grant non-statutory stock options, stock appreciation rights, restricted stock purchase rights or bonuses, restricted stock units, performance shares, performance units and cash-based awards or other stock based awards to any eligible participant.

| F-16 |

Bone Biologics Corporation

Notes to Unaudited Condensed Consolidated Financial Statements

The 2014 Stock Option Plan will be administered by our compensation committee. Subject to the provisions of our 2014 Stock Option Plan, the compensation committee determines, in its discretion, the persons to whom, and the times at which, awards are granted, as well as the size, terms and conditions of each award. All awards are evidenced by a written agreement between us and the holder of the award. The compensation committee has the authority to construe and interpret the terms of our 2014 Stock Option Plan and awards granted under our 2014 Stock Option Plan.

During the six months ended June 30, 2015 and 2014, the Company had stock-based compensation expenses of $137,412 and $-0-, respectively, related to issuances to the Company’s employees and directors, included in reported net loss. The total amount of stock-based compensation for the six months ended June 30, 2015 was related solely to the issuance of stock options.

A summary of stock option activity for the six months ended June 30, 2015, is presented below:

| Number | Weighted | ||||||||||||||||

| of Shares | Average | Weighted | |||||||||||||||

| Remaining | Exercise | Average | Aggregate | ||||||||||||||

| Subject to Exercise | Options | Price | Life (Years) | Value | |||||||||||||

| Outstanding as of January 1, 2014 | |||||||||||||||||

| Granted – 2014 | 757,977 | $ | 1.00 | 7.69 | - | ||||||||||||

| Forfeited – 2014 | - | - | - | - | |||||||||||||

| Exercised – 2014 | - | - | - | - | |||||||||||||

| Outstanding as of January 1, 2015 | 757,977 | $ | 1.00 | 7.44 | - | ||||||||||||

| Granted – 2015 | - | - | - | - | |||||||||||||

| Forfeited – 2015 | - | - | - | - | |||||||||||||

| Exercised – 2015 | - | - | - | - | |||||||||||||

| Outstanding as of June 30, 2015 | 757,977 | $ | 1.00 | 7.18 | - | ||||||||||||

| Date Issued | Exercise Price | Number of Shares | Expiration date | |||||||

| September 2014 | $ | 1.00 | 583,059 | September 18, 2021 | ||||||

| November 2014 | $ | 1.00 | 174,918 | November 3, 2024 | ||||||

| Total options at June 30, 2015 | 757,977 | |||||||||

The aggregate intrinsic value in the table above represents the total pre-tax intrinsic value (i.e., the difference between our closing stock price on the respective date and the exercise price, times the number of shares) that would have been received by the option holders had all option holders exercised their options. There have not been any options exercised during either the six months ended June 30, 2015 or the year ended December 31, 2014.

There were no options issued during the six months ended June 30, 2015. Vesting of options differs based on the terms of each option. The Company has valued the options at their date of grant utilizing the Black-Scholes option pricing model. As of the issuance of these consolidated financial statements, there was not an active public market for the Company’s shares. Accordingly, the fair value of the underlying options was determined based on the historical volatility data of similar companies, considering the industry, products and market capitalization of such other entities. The risk-free interest rate used in the calculations is based on the implied yield available on U.S. Treasury issues with an equivalent term approximating the expected life of the options as calculated using the simplified method. The expected life of the options used was based on the contractual life of the option granted. Stock-based compensation is a non-cash expense because we settle these obligations by issuing shares of our common stock from our authorized shares instead of settling such obligations with cash payments.

| F-17 |

Bone Biologics Corporation

Notes to Unaudited Condensed Consolidated Financial Statements

A summary of the changes in the Company’s non-vested options during the six months ended June 30, 2015, is as follows:

| Number of Non-vested Options |

Weighted Average Fair Value at Grant Date |

Intrinsic Value | ||||||||||

| Non-vested at January 1, 2014 | - | - | - | |||||||||

| Granted in 2014 | 757,977 | $ | 0.73 | |||||||||

| Vested in 2014 | 256,508 | $ | 0.73 | - | ||||||||

| Non-vested at January 1, 2015 | 501,469 | $ | 0.73 | - | ||||||||

| Vested in six months ended June 30, 2015 | - | $ | - | - | ||||||||

| Non-vested at June 30, 2015 | 501,469 | $ | 0.73 | - | ||||||||

| Exercisable at June 30, 2015 | 256,508 | $ | 0.73 | - | ||||||||

| Outstanding at June 30, 2015 | 757,977 | $ | 0.73 | - | ||||||||

As of June 30, 2015, total unrecognized compensation cost related to unvested stock options was $159,736. The cost is expected to be recognized over a weighted average period of 1.50 years.

10. Income Taxes

The Company’s effective tax rate is 0% for income tax for the six months ended June 30, 2015 and the Company expects that its effective tax rate for the full year 2015 will be 0%. Based on the weight of available evidence, including cumulative losses since inception and expected future losses, the Company has determined that it is more likely than not that the deferred tax asset amount will not be realized and therefore a valuation allowance has been provided on net deferred tax assets.

The Company files tax returns for U.S. Federal and the states of New Jersey and California. The Company is not currently subject to any income tax examinations. Since the Company’s inception, the Company had incurred losses from operations, which generally allows all tax years to remain open.

Uncertain Tax Positions

The Company recognizes the financial statement effects of a tax position when it becomes more likely than not, based upon the technical merits, that the position will be sustained upon examination.

The Company recognizes interest and/or penalties related to uncertain tax positions. To the extent accrued interest and penalties do not ultimately become payable, amounts accrued will be reduced and reflected in the period that such determination is made. The interest and penalties are recognized as other expense and not tax expense. The Company currently has no interest and penalties related to uncertain tax positions.

11. Related Party Transactions

Starting in September 2006, the Company entered into a series of consulting agreements with one of its stockholders whom previously served as chairman, president and CEO of the Company. The Company paid $75,000 and $70,000, for the six months ended June 30, 2015 and 2014, respectively, in consulting fees to this related party.

On September 19, 2014, the Company granted the consultant warrants to purchase up to 3% of the Company’s fully diluted shares of Common Stock outstanding as of the date of closing of the Merger totaling 699,671 shares of Common Stock of at a strike price of $1.00 per share, with a 7 year term to a consultant. The warrant will vest over a two year period from the effective date, with 33.33% of the shares subject to the warrant becoming vested and exercisable on the date that the consulting agreement is executed, 33.33% of the shares subject to the option becoming vested and exercisable on the date that is twelve (12) months after the effective date, and 33.34% of the shares subject to the warrant vesting and becoming exercisable on the date that is twenty four (24) months after the effective date. The initial fair value of the warrant was estimated at an aggregate value of $614,049, using the Black-Scholes option pricing model with the following assumptions at the date of issuance: expected volatility of 113.7%, risk-free interest rate of 2.29%, contractual term of 7 years and dividend yield of 0%. The fair value on the warrant was recorded as general and administrative expense and amortized over the term of the agreement. As of June 30, 2015, all costs associated with the warrants were recognized.

| F-18 |

Bone Biologics Corporation

Notes to Unaudited Condensed Consolidated Financial Statements

On February 29, 2015, the Company terminated the consulting contract. As per the contract, the consultant was provided a ninety (90) day notice and all warrants issued became fully vested.

In September 2014, the Company entered into a consulting agreement with MTF, which has agreed to provide the services of Mr. Michael Schuler to the Company as a contractor. Pursuant to the agreement, Mr. Schuler will serve as the Company’s Interim Chief Executive Officer for a period of 6 months. The agreement shall automatically renew for successive three (3) month periods unless either party provides written notice to the other party at least 10 days in advance of the renewal term of its decision not to renew the term. The agreement is intended to be temporary in nature and will cease once the Company retains a permanent Chief Executive Officer. There are no payments due to MTF or Mr. Schuler with respect to any change in control of the Company or termination of the consulting agreement. For the six months ended June 30, 2015, the Company recognized $90,000 of expense related to this contract.

See Note 6 for related party notes payable to MTF.

12. Subsequent Events

Employment Agreements

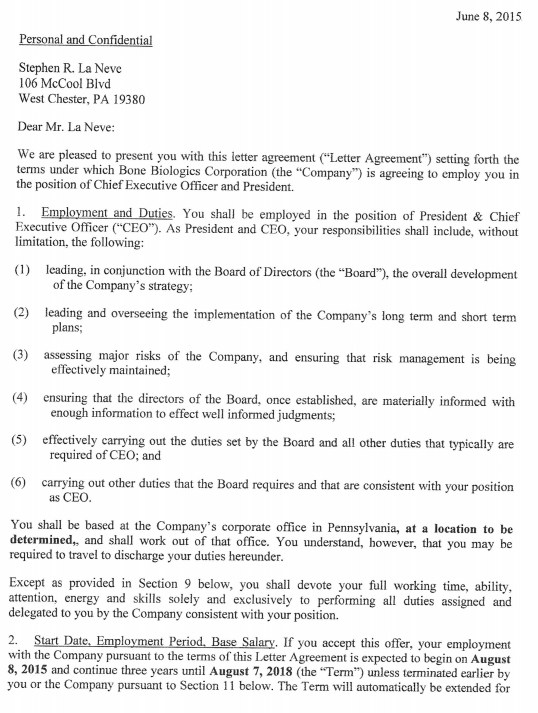

Bone Biologics Corporation., a Delaware corporation (the “Company”) appointed Mr. Stephen R. La Neve, age 56, as the Company’s Chief Executive Officer and President, and Mr. Jeff Frelick, age 50, as the Company’s Chief Operating Officer, each to be effective on August 17, 2015 (the “Effective Date”).

Steve La Neve brings thirty years of health care experience, leadership and success to Life Science Enterprises. Prior to his current position, Steve held leadership roles in the device and diagnostic segments which include: CEO and president of Etex Corporation; president of Becton Dickinson’s Pre-Analytical Systems business; president of Medtronic’s $3.5b Spine and Biologics business; and president of Medtronic’s second largest country business unit, Medtronic Japan. He also served as senior vice president and executive vice president at Premier, one of the largest GPOs in the United States and ran the global Injection Systems business unit for Becton Dickinson. Additionally, Steve has held a number of commercial leadership roles at Becton Dickinson, Roche Diagnostics and E Merck Diagnostic Systems in sales, marketing, strategic planning and project management both in the US and outside the US. He serves on the board of directors for SkelRegen, LLC and Rapid Pathogen Screening, Inc. (RPS), and he consults for private equity companies in the medical device area. Steve holds a B.S. in Health Planning and Administration from the Pennsylvania State University, an M.B.A. from West Chester University, and is a member of the omicron delta epsilon honor society for academic excellence in economics.

Jeffrey Frelick is the COO of Life Science Enterprises, where he brings more than 25 years of med-tech experience. He spent the past 15 years on Wall Street as a sell-side analyst following the med-tech industry at investment banks such as Canaccord Genuity, ThinkEquity and Lazard. Prior to becoming an equity research analyst, Jeff worked at Boston Biomedical Consultants where he provided strategic planning assistance, market research data and due diligence for diagnostics companies. He previously held sales and sales management positions at Becton Dickinson’s Primary Care Diagnostic Division after gaining technical experience as a laboratory technologist with Clinical Pathology Facility. Jeff received a B.S. in Biology from University of Pittsburgh and an M.B.A. from Suffolk University’s Sawyer Business School.

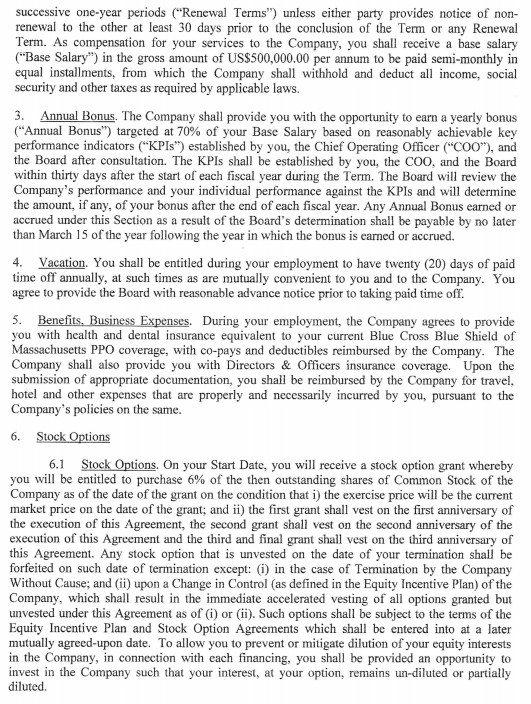

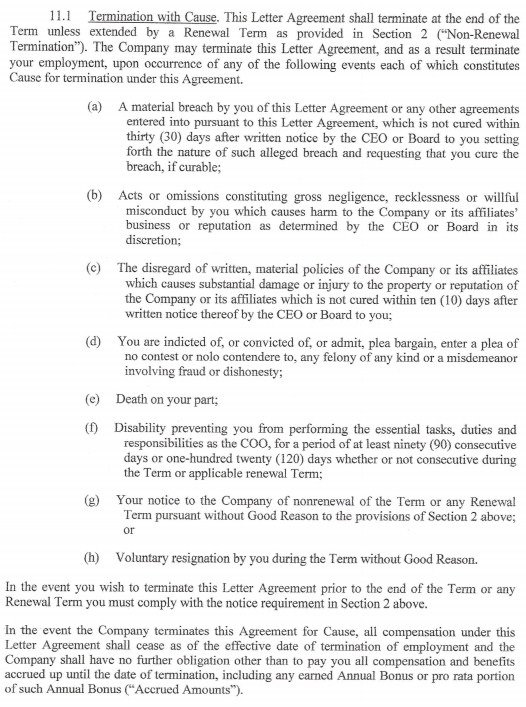

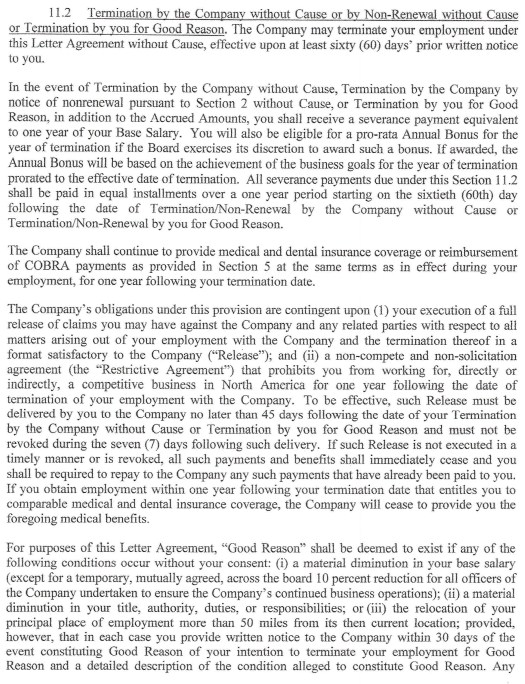

Pursuant to the employment agreement entered into between the Company and Mr. La Neve on June 8, 2015, the initial term of his employment shall begin on August 17, 2015 and continue for three years until August 16, 2018, which term will automatically be extended for successive one year periods, unless earlier terminated. Mr. La Neve shall receive a base salary in the gross amount of $500,000 per annum to be paid semi-monthly in equal installments. In addition, Mr. La Neve is eligible to earn a yearly bonus targeted at 70% of the base salary based on reasonably achievable key performance indicators established by Mr. La Neve, the Company’s Chief Operating Officer and the Board of Directors after consultation. On Mr. La Neve’s start date, he will receive an option to purchase 6% of the then outstanding shares of the Company’s common stock, at an exercise price that equals to the fair market price on the date of the grant. These options will vest annually over three (3) years such that they are vested in full on the third year anniversary of the employment agreement date, provided, that any stock option that is unvested on the date of termination shall be forfeited on such date of termination, subject to certain exceptions. If Mr. La Neve is terminated by the Company Without Cause, or by Non-Renewal Without Cause, or terminated for Good Reason (each as described in the employment agreement), Mr. La Neve shall receive a severance payment equivalent to one year of base salary, and shall also be eligible for a pro-rata annual bonus for the year of termination if the Board of Directors exercise its discretion to award such a bonus. All severance payments will be paid in equal installments over a one year period starting on the sixtieth day following the termination. The severance payment will be contingent upon Mr. La Neve’s execution of a full release of claims against the Company and a non-compete and non-solicitation agreement as provided in the employment agreement.

Pursuant to the employment agreement entered into between the Company and Mr. Frelick on June 8, 2015, the initial term of his employment shall begin on August 17, 2015 and continue for three years until August 16, 2018, which term will automatically be extended for successive one year periods, unless earlier terminated. Mr. Frelick shall receive a base salary in the gross amount of $300,000 per annum to be paid semi-monthly in equal installments. In addition, Mr. Frelick is eligible to earn a yearly bonus targeted at 50% of the base salary based on reasonably achievable key performance indicators established by Mr. Frelick, the Company’s Chief Executive Officer and the Board of Directors after consultation. On Mr. Frelick’s start date, he will receive an option to purchase 3% of the then outstanding shares of the Company’s common stock, at an exercise price that equals to the fair market price on the date of the grant. These options will vest annually over three (3) years such that they are vested in full on the third year anniversary of the employment agreement date, provided, that any stock option that is unvested on the date of termination shall be forfeited on such date of termination, subject to certain exceptions. If Mr. Frelick is terminated by the Company Without Cause, or by Non-Renewal Without Cause, or terminated for Good Reason (each as described in the employment agreement), Mr. Frelick shall receive a severance payment equivalent to one year of base salary, and shall also be eligible for a pro-rata annual bonus for the year of termination if the Board of Directors exercise its discretion to award such a bonus. All severance payments will be paid in equal installments over a one year period starting on the sixtieth day following the termination. The severance payment will be contingent upon Mr. Frelick’s execution of a full release of claims against the Company and a non-compete and non-solicitation agreement as provided in the employment agreement.

| F-19 |

Bone Biologics Corporation

Notes to Unaudited Condensed Consolidated Financial Statements

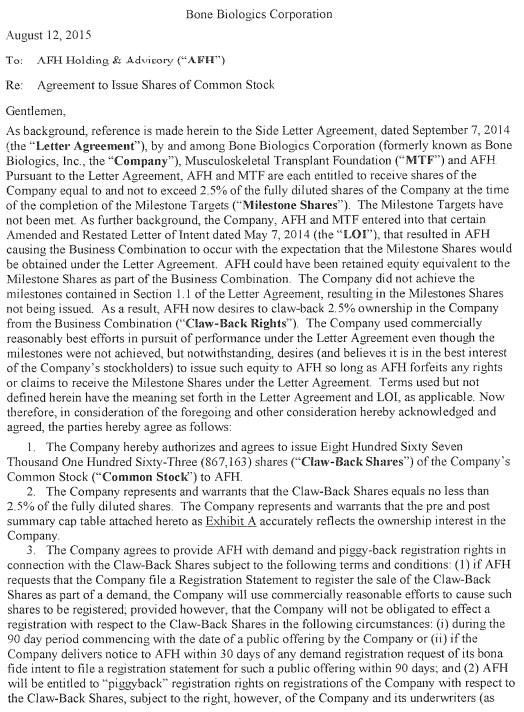

AFH Revised Milestone Side Letter Agreement

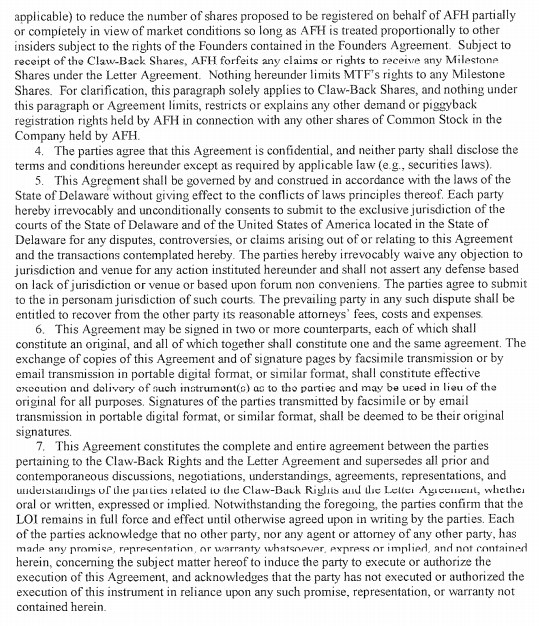

On August 11, 2015 the Company entered into the Letter Agreement, by and between, Bone Biologics Corporation and AFH to amend the Side Letter Agreement, dated September 7, 2014 (the “Letter Agreement”), by and among Bone Biologics (formerly known as Bone Biologics, Inc.) MTF and AFH. Pursuant to the Letter Agreement, AFH and MTF are each entitled to receive shares of the Company equal to and not to exceed 2.5% of the fully diluted shares of the Company at the time of the completion of the Milestone Targets (“Milestone Shares”). The Milestone Targets have not been met. The Company used commercially reasonably best efforts in pursuit of performance under the Letter Agreement even though the milestones were not achieved, but notwithstanding, desires (and believes it is in the best interest of the Company’s stockholders) to issue such equity, Eight Hundred Sixty Seven Thousand One Hundred Sixty-Three (867,163) Common Shares, to AFH so long as AFH forfeits any rights or claims to receive the Milestone Shares under the Letter Agreement.

MTF Revised Milestone Side Letter Agreement