UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

[X] ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended September 30, 2019

OR

[ ] TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

Commission file number: 333-163439

WALL STREET MEDIA CO, INC.

(Exact name of registrant as specified in its charter)

| Nevada | 26-4170100 | |

(State or other jurisdiction of incorporation or organization) |

(I.R.S.

Employer Identification No.) |

110 Front Street, Suite 300 Jupiter, FL |

33477 | |

| (Address of principal executive offices) | (Zip Code) |

(561) 240-0333

(Registrant’s telephone number, including area code)

Securities registered under Section 12(b) of the Act: None

Securities registered under Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes [ ] No [X]

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes [ ] No [X]

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes [X] No [ ]

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes [X] No [ ]

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. [ ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer [ ] | Accelerated filer [ ] |

| Non-accelerated filer [ ] | Smaller reporting company [X] |

| (Do not check if a smaller reporting company) | |

| Emerging growth company [ ] |

If an emerging growth company, indicate by check mark whether the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. [ ]

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes [ ] No [X]

State the aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of the last business day of the registrant’s most recently completed second fiscal quarter.

As of March 31, 2019, the aggregate market value of the registrant’s voting and non-voting common stock held by non-affiliates of the registrant was $1,638,609 based on the last reported sale price of our common stock on the OTCQB, which was $0.24 per share on March 31, 2019.

As of October 31, 2019, there were 26,922,007 shares of the registrant’s common stock issued and outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

None.

INDEX

CERTAIN CAUTIONARY STATEMENTS REGARDING FORWARD-LOOKING INFORMATION

Certain statements in this annual report on Form 10-K contain or may contain forward-looking statements that are subject to known and unknown risks, uncertainties and other factors which may cause actual results, performance or achievements to be materially different from any future results, performance or achievements expressed or implied by such forward-looking statements. These forward-looking statements were based on various factors and were derived utilizing numerous assumptions and other factors that could cause the Company’s actual results to differ materially from those in the forward-looking statements. These factors include, but are not limited to, economic, political and market conditions and fluctuations, government and industry regulation, interest rate risk, U.S. and global competition, and other factors. Most of these factors are difficult to predict accurately and are generally beyond the Company’s control. You should consider the areas of risk described in connection with any forward-looking statements that may be made herein. Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date of this report. Readers should carefully review this report in its entirety, including but not limited to the financial statements and the notes thereto. Except for our ongoing obligations to disclose material information under the Federal securities laws, the Company undertakes no obligation to release publicly any revisions to any forward-looking statements, to report events or to report the occurrence of unanticipated events.

When used in this annual report on Form 10-K, the terms “Wall Street Media”, “Company”, “we,” “our,” and “us” refers to Wall Street Media Co, Inc.

Company Overview

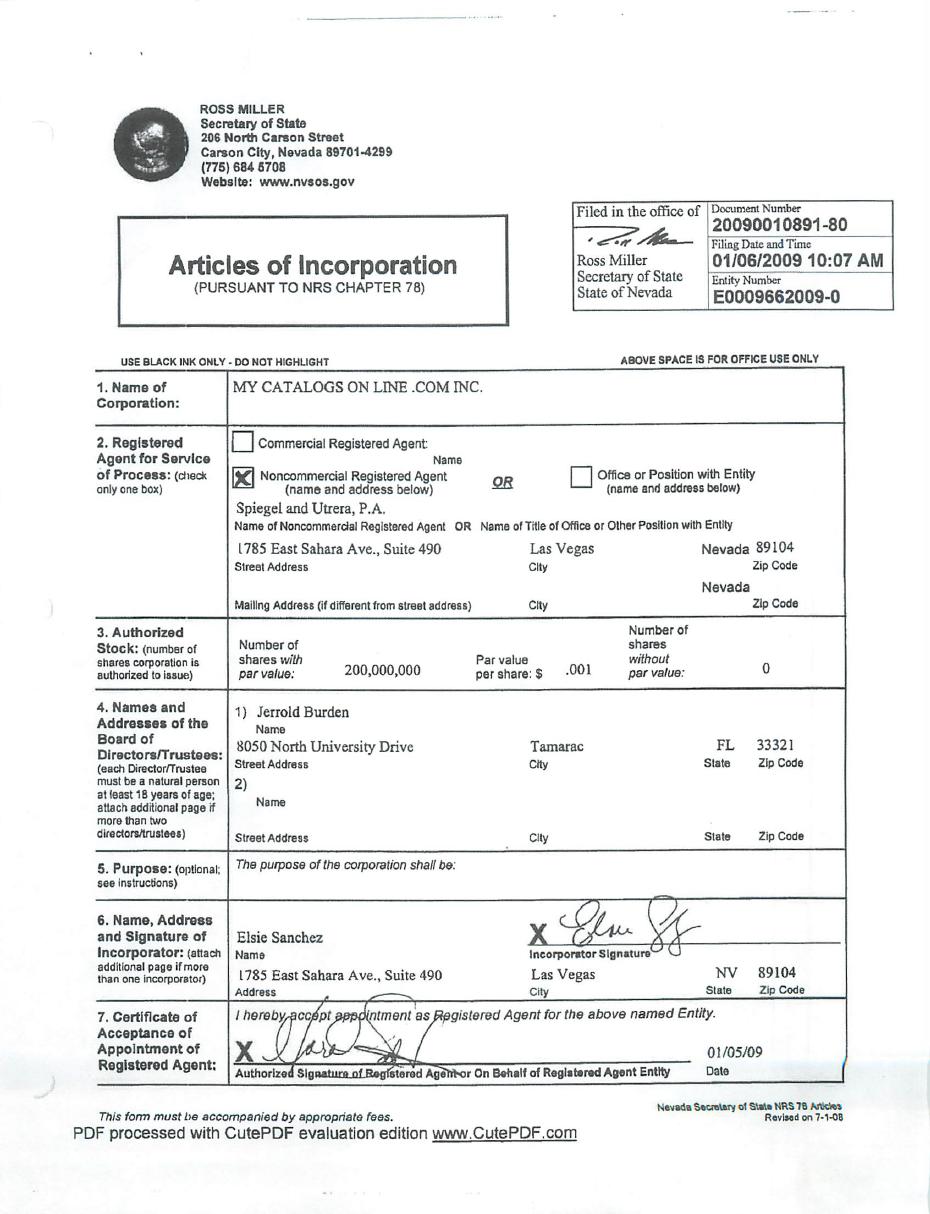

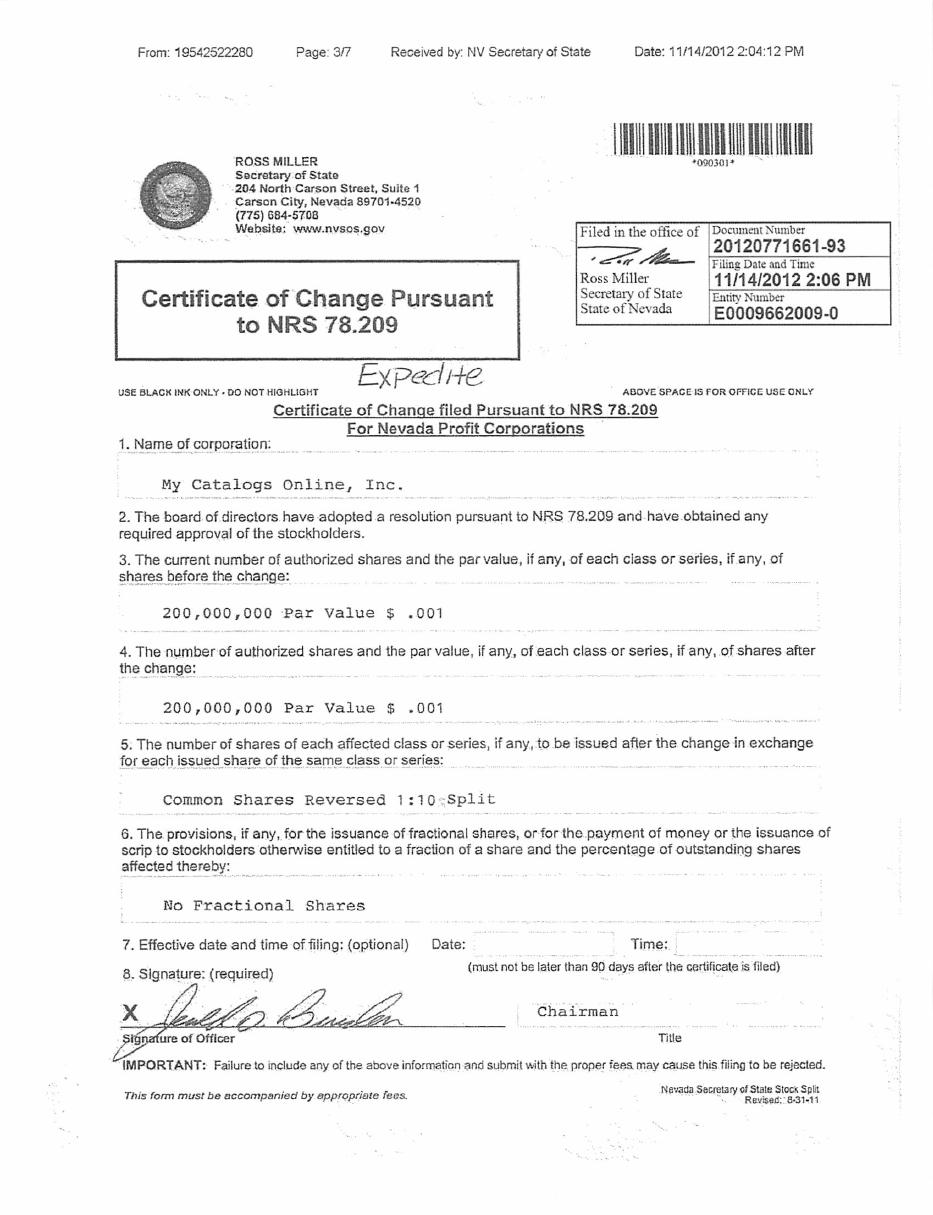

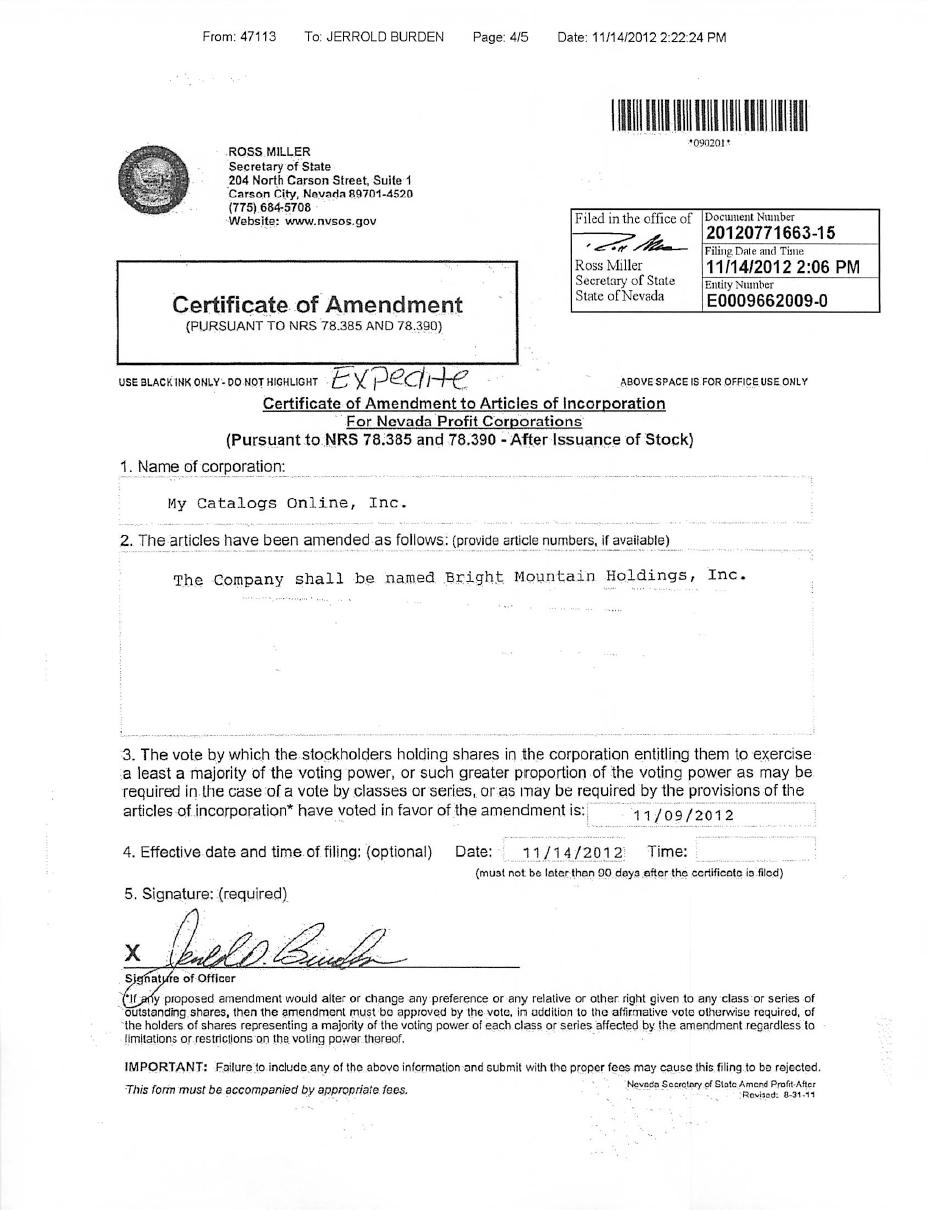

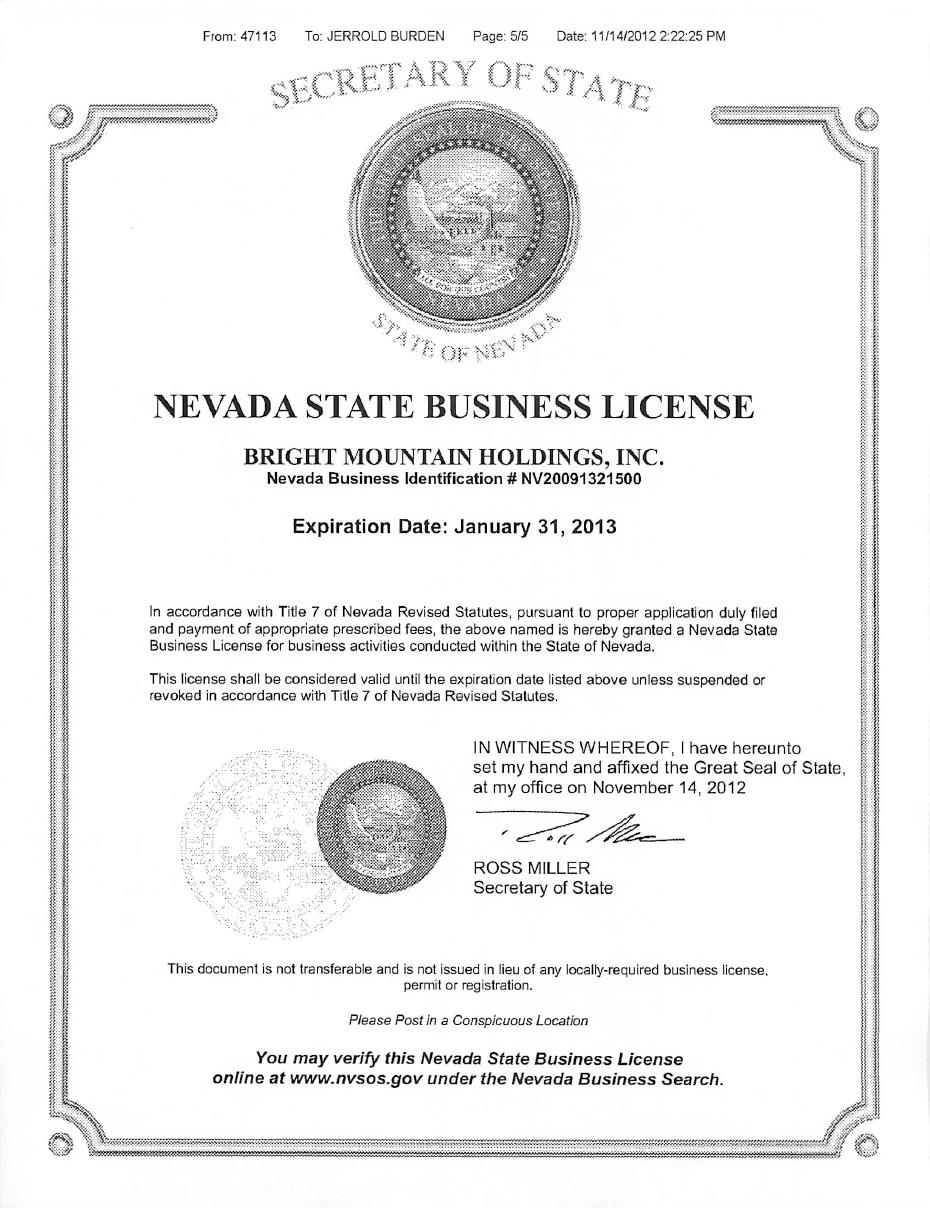

Wall Street Media Co, Inc. (the “Company”, “we”, “us”, “our”) was organized as Mycatalogsonline.com, Inc. in the state of Nevada on January 6, 2009. In April 2009, the Company changed its name to My Catalogs Online, Inc. In August 2013 changed its name to Wall Street Media Co, Inc.

The Company provides consulting and management services to entities looking to merge with or acquire or otherwise consult with third party entities. These services are currently provided to Landmark-Pegasus, Inc., a related party (“Landmark-Pegasus”). Landmark-Pegasus is owned by John Moroney, the Company’s majority shareholder. Mr. Moroney also acts as Landmark-Pegasus’ President.

Marketing Strategy

The Company plans to increase its current client base by exploiting its relationship with Landmark-Pegasus, a related party.

An investment in our common stock is highly speculative, involves a high degree of risk, and should be made only by investors who can afford a complete loss. You should carefully consider the following risk factors, together with the other information in this annual report on Form 10-K, including our financial statements and the related notes, before you decide to buy our common stock. If any of the following risks actually occur, our business, financial condition, or results of operations could be materially adversely affected, the trading of our common stock could decline, and you may lose all or part of your investment therein.

| 1 |

Risks Relating to the Early Stage of our Company

We are at a very early operational stage, our success is subject to the substantial risks inherent in the establishment of a new business venture, and 100% of revenues are from a related party.

The implementation of our business strategy, particularly our consulting service business, is in a very early stage. Our business and operations should be considered to be in a very early stage and subject to all of the risks inherent in the establishment of a new business venture. Accordingly, our intended business and operations may not prove to be successful in the near future, if at all. Any future success that we might enjoy will depend upon many factors, several of which may be beyond our control, or which cannot be predicted at this time, and which could have a material adverse effect upon our financial condition, business prospects and operations and the value of an investment in our Company.

For the fiscal years ended September 30, 2019 and 2018, $90,290 and $56,000, or 100%, respectively, of the Company’s revenue was derived from Landmark-Pegasus, a related party. Landmark-Pegasus is wholly owned by John Moroney, who beneficially owns approximately 59.8% of the Company’s common stock. Mr. Moroney also acts as Landmark-Pegasus’ President and is Landmark-Pegasus’ sole director. Currently, the Company’s services are provided solely to Landmark-Pegasus and to a client of Landmark-Pegasus.

We have a very limited operating history and our business plan is unproven and may not be successful.

To date, we have not provided, licensed or sold any substantial amount of services and do not have any definitive agreements to do so. We have not proven that our business model will allow us to generate a profit. In addition, we currently provide all of our consulting services to Landmark-Pegasus, a related party. For the fiscal years ended September 30, 2019 and 2018, $90,290 and $56,000, or 100%, respectively, of the Company’s revenue was derived from Landmark-Pegasus. Landmark-Pegasus is wholly owned by John Moroney, who beneficially owns approximately 59.8% of the Company’s common stock. Mr. Moroney also acts as Landmark-Pegasus’ President and is Landmark-Pegasus’ sole director. Currently, the Company’s services are provided solely to Landmark-Pegasus and to a client of Landmark-Pegasus.

We have suffered operating losses since inception and we may not be able to achieve profitability.

We had an accumulated deficit of $1,419,761 as of September 30, 2019 and we expect to continue to incur significant developmental expenses in the foreseeable future related to development of our consulting services business. As a result, we are sustaining substantial operating and net losses, and it is possible that we will never be able to sustain or develop the revenue levels necessary to attain profitability.

We may have difficulty raising additional capital, which could deprive us of necessary resources.

We will need to raise additional funds through public or private debt or equity financing, collaborative relationships or other arrangements. Our ability to raise additional financing depends on many factors beyond our control, including the state of capital markets and the market price of our common stock. Because our common stock is not listed on a national securities exchange, such as the New York Stock Exchange (“NYSE”) or The NASDAQ Stock Market (“NASDAQ”), many investors may not be willing or allowed to purchase it or may demand steep discounts. Sufficient additional financing may not be available to us or may be available only on terms that would result in substantial dilution to the current owners of our common stock.

We expect to pursue additional capital during the fiscal year ending September 30, 2019, but we do not have any firm commitments for funding. If we are unsuccessful in raising additional capital, or the terms of raising such capital are unacceptable, we may have to modify our business plan and/or significantly curtail our planned activities and other operations.

| 2 |

There are substantial doubts about our ability to continue as a going concern and if we are unable to continue our business, our shares may have little or no value.

The Company’s ability to become a profitable operating company is dependent upon its ability to generate revenues and/or obtain financing adequate to support our cost structure. There can be no assurance that we will generate revenues or financing. These factors have raised substantial doubts about our ability to continue as a going concern. We plan to attempt to raise additional equity capital by selling shares through one or more private placement or public offerings. However, the doubts raised, relating to our ability to continue as a going concern, may make our shares an unattractive investment for potential investors. These factors, among others, may make it difficult to raise any additional capital.

Failure to effectively manage our growth could place strains on our managerial, operational and financial resources and could adversely affect our business and operating results.

Any future growth by us, or an increase in the number of our strategic relationships will create a strain on our managerial, operational and financial resources. This strain may inhibit our ability to achieve the rapid execution necessary to implement our business plan, and could have a material adverse effect upon our financial condition, business prospects and operations and the value of an investment in our Company.

Risks Relating to Our Business

We will need to achieve commercial acceptance of our consulting services to generate revenues and achieve profitability.

We may not successfully develop successful relationships with potential clients, and even if we do, we may not do so on a timely basis. We cannot predict when significant commercial market acceptance for our consulting services will develop, if at all, and we cannot reliably estimate the projected size of any such potential market. If markets fail to accept our consulting services, we may not be able to generate revenues from the provision of such services. Our revenue growth and achievement of profitability will depend substantially on our ability to introduce services that are accepted by customers. If we are unable to cost-effectively achieve acceptance of our services by customers, or if the associated services do not achieve wide market acceptance, our business will be materially and adversely affected.

We will need to establish additional relationships with collaborative and development partners to fully develop and market our services.

We do not possess all of the resources necessary to develop and commercialize consulting services on a mass scale. Unless we expand our development capacity and enhance our internal marketing, we will need to make appropriate arrangements with collaborative partners to develop and commercialize consulting services.

Collaborations may allow us to:

| ● | generate cash flow and revenue; | |

| ● | offset some of the costs associated with our internal development; and | |

| ● | successfully commercialize consulting services. |

If we need, but do not find, appropriate partner arrangements, our ability to develop and commercialize consulting services could be adversely affected. Even if we are able to find collaborative partners, the overall success of the development and commercialization of our services will depend largely on the efforts of other parties and is beyond our control. In addition, in the event we pursue our commercialization strategy through collaboration, there are a variety of attendant technical, business and legal risks, including:

● a development partner would likely gain access to our proprietary information and knowledge, potentially enabling the partner to develop services without us or design around our intellectual property;

● We may not be able to control the amount and timing of resources that our collaborators may be willing or able to devote to the development or commercialization of services, or to their marketing and distribution; and

● Disputes may arise between us and our collaborators that result in the delay or termination of the development or commercialization of our services or that result in costly litigation or arbitration that diverts our management’s resources.

| 3 |

The occurrence of any of the above risks could impair our ability to generate revenues and harm our business and financial condition.

We may not be successful at marketing our consulting services.

We may not be able to market our services, or efforts we exert to develop, commercialize or promote such services may not result in revenue or earnings.

We may lose out to larger and better-established competitors.

The consulting services industry is intensely competitive. Most of our competitors have significantly greater financial, technical, marketing and distribution resources, as well as greater experience in the industry than we have. Our services may not be competitive with their services. If this happens, our sales and revenues will decline. In addition, our current and potential competitors may establish cooperative relationships with larger companies, to gain access to greater development or marketing resources. Competition may result in price reductions, reduced gross margins and loss of market share.

Risks Relating to our Stock

Trading on the OTC Markets is volatile, sporadic and often thin, which could depress the market price of our common stock and make it difficult for our stockholders to resell their common stock.

Our common stock is quoted on the OTCQB tier of the OTC Markets. Trading in securities quoted on the OTC Markets is often thin and characterized by wide fluctuations in trading prices, due to many factors, some of which may have little to do with our operations or business prospects. This volatility could depress the market price of our common stock for reasons unrelated to operating performance. Moreover, the OTC Markets is not a stock exchange, and trading of securities on the OTC Markets is often more sporadic than the trading of securities listed on a stock exchange like NASDAQ or the NYSE. Our common stock has a history of thin trading. During the 52-week period ended December 17, 2018, trades were only reported on 13 trading days. These factors may result in investors having difficulty reselling any shares of our common stock.

Our common stock price is likely to be highly volatile because of several factors, including a limited public float.

The market price of our common stock has been volatile in the past. For example, as of October 01, 2019, our common stock has had a 52-week high sale price of $0.24 and a low sale price of $0.12. The market price of our common stock is likely to be highly volatile in the future, as well. You may not be able to resell shares of our common stock following periods of volatility because of the market’s adverse reaction to volatility.

Other factors that could cause such volatility may include, among other things:

| ● | actual or anticipated fluctuations in our operating results; | |

| ● | the absence of securities analysts covering us and distributing research and recommendations about us; | |

| ● | we may have a low trading volume for a number of reasons, including that a large portion of our stock is closely held; | |

| ● | overall stock market fluctuations; | |

| ● | announcements concerning our business or those of our competitors; | |

| ● | actual or perceived limitations on our ability to raise capital when we require it, and to raise such capital on favorable terms; |

| 4 |

| ● | conditions or trends in the industry; | |

| ● | litigation; | |

| ● | changes in market valuations of other similar companies; | |

| ● | future sales of common stock; | |

| ● | departure of key personnel or failure to hire key personnel; and | |

| ● | general market conditions. |

Any of these factors could have a significant and adverse impact on the market price of our common stock. In addition, the stock market in general has at times experienced extreme volatility and rapid decline that has often been unrelated or disproportionate to the operating performance of particular companies. These broad market fluctuations may adversely affect the trading price of our common stock, regardless of our actual operating performance.

Future stock issuances would dilute stockholders’ ownership, and may reduce our share value.

If, in the future, we issue additional shares, the future issuance of common stock or preferred stock may result in substantial dilution in the percentage of our common stock held by our then existing shareholders. We may value any common stock issued in the future on an arbitrary basis. The issuance of common stock for future services or acquisitions or other corporate actions may have the effect of diluting the value of the shares held by our investors, and might have an adverse effect on any trading market for our common stock.

We face corporate governance risks and negative investor perceptions because we have only one officer and director and have not adopted a written policy for the review, approval or ratification of transactions with related parties or conflicted parties.

Mr. Lubchansky is our sole officer and director. As such, he has significant control over our business direction. Additionally, because he is our sole director, there are no other board members available to second and/or approve related party transactions involving Mr. Lubchansky, including the compensation Mr. Lubchansky may be paid. Additionally, there is no segregation of duties between officers because Mr. Lubchansky is our sole officer, and as such, he is solely responsible for the oversight of our accounting functions. Because no other directors are approving our financial statements, investors may question the accuracy of financial statements. The price of our common stock may be adversely affected and/or devalued compared to similarly sized companies with multiple officers and directors due to the investing public’s perception of limitations facing our company due to the fact that we only have one officer and director.

Our common stock is currently, has been in the past, and may be in the future, a “penny stock” under SEC rules. It may be more difficult to resell securities classified as “penny stock.”

Our common stock is a “penny stock” under applicable SEC rules (generally defined as non-exchange traded stock with a per-share price below $5.00). Unless we obtain a per-share price above $5.00, these rules impose additional sales practice requirements on broker-dealers that recommend the purchase or sale of penny stocks to persons other than those who qualify as “established customers” or “accredited investors.” For example, broker-dealers must determine the appropriateness for non-qualifying persons of investments in penny stocks. Broker-dealers must also provide, prior to a transaction in a penny stock not otherwise exempt from the rules, a standardized risk disclosure document that provides information about penny stocks and the risks in the penny stock market. The broker-dealer also must provide the customer with current bid and offer quotations for the penny stock, disclose the compensation of the broker-dealer and its salesperson in the transaction, furnish monthly account statements showing the market value of each penny stock held in the customer’s account, provide a special written determination that the penny stock is a suitable investment for the purchaser, and receive the purchaser’s written agreement to the transaction.

| 5 |

Legal remedies available to an investor in “penny stocks” may include the following:

| ● | If a “penny stock” is sold to the investor in violation of the requirements listed above, or other federal or states securities laws, the investor may be able to cancel the purchase and receive a refund of the investment. | |

| ● | If a “penny stock” is sold to the investor in a fraudulent manner, the investor may be able to sue the persons and firms that committed the fraud for damages. |

However, investors who have signed arbitration agreements may have to pursue their claims through arbitration.

These requirements may have the effect of reducing the level of trading activity, if any, in the secondary market for a security that becomes subject to the penny stock rules. The additional burdens imposed upon broker-dealers by such requirements may discourage broker-dealers from effecting transactions in our securities, which could severely limit the market price and liquidity of our securities. These requirements may restrict the ability of broker-dealers to sell our common stock and may affect your ability to resell our common stock.

Many brokerage firms will discourage or refrain from recommending investments in penny stocks. Most institutional investors will not invest in penny stocks. In addition, many individual investors will not invest in penny stocks due, among other reasons, to the increased financial risk generally associated with these investments.

For these reasons, penny stocks may have a limited market and, consequently, limited liquidity. We can give no assurance that our common stock will not remain classified as a “penny stock” in the future.

If we fail to maintain effective internal control over financial reporting, the price of our securities may be adversely affected.

Our internal control over financial reporting may have weaknesses and conditions that could require correction or remediation, the disclosure of which may have an adverse impact on the price of our common stock. We are required to establish and maintain appropriate internal control over financial reporting. Failure to establish those controls, or any failure of those controls once established, could adversely affect our public disclosures regarding our business, prospects, financial condition or results of operations. In addition, management’s assessment of internal control over financial reporting may identify weaknesses and conditions that need to be addressed in our internal control over financial reporting or other matters that may raise concerns for investors. Any actual or perceived weaknesses and conditions that need to be addressed in our internal control over financial reporting or disclosure of management’s assessment of our internal control over financial reporting may have an adverse impact on the price of our common stock.

We are required to comply with certain provisions of Section 404 of the Sarbanes-Oxley Act of 2002, as amended (the “Sarbanes-Oxley Act”) and if we fail to continue to comply, our business could be harmed and the price of our securities could decline.

Rules adopted by the SEC pursuant to Section 404 of the Sarbanes-Oxley Act require an annual assessment of internal control over financial reporting, and for certain issuers (but not us) an attestation of this assessment by the issuer’s independent registered public accounting firm. The standards that must be met for management to assess the internal control over financial reporting as effective are evolving and complex, and require significant documentation, testing, and possible remediation to meet the detailed standards. We expect to incur significant expenses and to devote resources to Section 404 compliance on an ongoing basis. It is difficult for us to predict how long it will take or costly it will be to complete the assessment of the effectiveness of our internal control over financial reporting for each year and to remediate any deficiencies in our internal control over financial reporting. As a result, we may not be able to complete the assessment and remediation process on a timely basis. In the event that our Chief Executive Officer or principal financial officer determines that our internal control over financial reporting is not effective as defined under Section 404, we cannot predict how regulators will react or how the market prices of our securities will be affected; however, we believe that there is a risk that investor confidence and the market value of our securities may be negatively affected.

| 6 |

Shares eligible for future sale may adversely affect the market.

From time to time, certain of our stockholders may be eligible to sell all or some of their shares of common stock by means of ordinary brokerage transactions in the open market pursuant to Rule 144 promulgated under the Securities Act, subject to certain limitations. In general, pursuant to Rule 144, non-affiliate stockholders may sell freely after six months, subject only to the current public information requirement. Affiliates may sell after six months, subject to the Rule 144 volume, manner of sale (for equity securities), current public information, and notice requirements. Given the limited trading of our common stock, resale of even a small number of shares of our common stock pursuant to Rule 144 or an effective registration statement may adversely affect the market price of our common stock.

The Financial Industry Regulatory Authority (“FINRA”) sales practice requirements may also limit a stockholder’s ability to buy and sell our stock.

In addition to the penny stock rules discussed above, FINRA rules require that in recommending an investment to a customer, a broker -dealer must have reasonable grounds for believing that the investment is suitable for that customer. Prior to recommending speculative, low-priced securities to their non-institutional customers, broker-dealers must make reasonable efforts to obtain information about the customer’s financial status, tax status, investment objectives and other information. Under interpretations of these rules, FINRA believes that there is a high probability that speculative low-priced securities will not be suitable for at least some customers. FINRA requirements make it more difficult for broker-dealers to recommend that their customers buy our common stock, which may limit the ability to buy and sell our stock and have an adverse effect on the market value for our shares.

An investor’s ability to trade our common stock may be limited by trading volume.

The Company’s shares are currently quoted on the OTCQB under the symbol, “WSCO.” An active trading market for our common stock has not developed, and may not develop, on the OTCQB. During the 52-week period ended October 11, 2019, trades were only reported on 28 trading days. A limited trading volume may prevent our shareholders from selling shares at such times or in such amounts as they may otherwise desire.

Our Company has a concentration of stock ownership and control, which may have the effect of delaying, preventing, or deterring a change of control.

Our common stock ownership is highly concentrated. Through ownership of shares of our common stock, one shareholder, John Moroney, beneficially owns approximately 59.8% of our total outstanding shares of common stock. As a result of the concentrated ownership of the stock, this stockholder, acting alone, will be able to control all matters requiring stockholder approval, including the election of directors and approval of mergers and other significant corporate transactions. This concentration of ownership may have the effect of delaying, preventing or deterring a change in control of our Company. It could also deprive our stockholders of an opportunity to receive a premium for their shares as part of a sale of our Company and it may affect the market price of our common stock.

We have not voluntarily implemented various corporate governance measures, in the absence of which, shareholders may have more limited protections against interested director transactions, conflicts of interest and similar matters.

Federal legislation, including the Sarbanes-Oxley Act, has resulted in the adoption of various corporate governance measures designed to promote the integrity of the corporate management and the securities markets. Some of these measures have been adopted in response to legal requirements; others have been adopted by companies in response to the requirements of national securities exchanges, such as the NYSE or NASDAQ, on which their securities are listed. Among the corporate governance measures that are required under the rules of national securities exchanges, are those that address the Board of Directors’ independence, audit committee oversight, and the adoption of a code of ethics. While our Board of Directors has adopted a Code of Ethics, we have not yet adopted any of these corporate governance measures, and since our securities are not listed on a national securities exchange, we are not required to do so. It is possible that if we were to adopt some or all of these corporate governance measures, shareholders would benefit from somewhat greater assurances that internal corporate decisions were being made by disinterested directors and that policies had been implemented to define responsible conduct. For example, in the absence of audit, nominating and compensation committees comprised of at least a majority of independent directors, decisions concerning matters such as compensation packages to our senior officers and recommendations for director nominees, may be made by a majority of directors who have an interest in the outcome of the matters being decided. Prospective investors should bear in mind our current lack of corporate governance measures in formulating their investment decisions.

| 7 |

Because we will not pay dividends in the foreseeable future, stockholders will only benefit from owning common stock if it appreciates.

We have never paid dividends on our common stock and we do not intend to do so in the foreseeable future. We intend to retain any future earnings to finance our growth. Accordingly, any potential investor who anticipates the need for current dividends from his investment should not purchase our common stock.

ITEM 1B. UNRESOLVED STAFF COMMENTS

Not applicable.

The Company leases on a month to month basis virtual office space at 110 Front Street – Suite 300, Jupiter, FL 33477. Monthly rent is $125.

From time to time, we may become involved in various lawsuits and legal proceedings which arise in the ordinary course of business. However, litigation is subject to inherent uncertainties, and an adverse result in these or other matters may arise from time to time that may harm our business. We are currently not aware of any such legal proceedings or claims that we believe will have, individually or in the aggregate, a material adverse effect on our business, financial condition or operating results

ITEM 4. MINE SAFETY DISCLOSURES

Not applicable.

ITEM 5. MARKET FOR COMMON EQUITY AND RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

Market Information

Our common stock is quoted on the OTCQB market tier of the OTC Markets Group under the symbol “WSCO.” Securities quoted on the OTCQB trade via a dealer network, as opposed to trading on a centralized stock exchange, such as the NYSE. In order to have securities quoted on the OTCQB, a company must be current in its financial reporting, but it is not subject to any minimum financial requirements and listing standards, as is the case with national securities exchanges. Trading in OTCQB stocks can be volatile, sporadic and risky, as thinly traded stocks tend to move more rapidly in price than more liquid securities. Such trading may also depress the market price of our common stock and make it difficult for our stockholders to resell their common stock.

| 8 |

The following table sets forth, as reported by the OTCQB, the per share high and low bid quotations for our common stock for each of the periods indicated. These quotations reflect inter-dealer prices, without retail mark-up, mark-down or commission and may not necessarily represent actual transactions. The data in the table below presents historical information only and is not intended to predict future sale prices of our common stock. Trading in securities, such as our common stock, on the OTC Markets may be volatile and thin and characterized by wide fluctuations in trading prices. See “Risk Factors—Trading on the OTC Markets is volatile, sporadic and often thin, which could depress the market price of our common stock and make it difficult for our security holders to resell their common stock.”

| High | Low | |||||||

| Fiscal Year Ended September 30, 2018 | ||||||||

| Quarter Ended December 31, 2017 | $ | 0.3000 | $ | 0.0200 | ||||

| Quarter Ended March 31, 2018 | 0.2070 | 0.0700 | ||||||

| Quarter Ended June 30, 2018 | 0.2000 | 0.0500 | ||||||

| Quarter Ended September 30, 2018 | 0.0200 | 0.1500 | ||||||

| Fiscal Year Ended September 30, 2019 | ||||||||

| Quarter Ended December 31, 2018 | $ | 0.1970 | $ | 0.1800 | ||||

| Quarter Ended March 31, 2019 | 0.1970 | 0.1190 | ||||||

| Quarter Ended June 30, 2019 | 0.2400 | 0.1190 | ||||||

| Quarter Ended September 30, 2019 | $ | 0.1800 | $ | 0.1190 | ||||

**On October 11, 2019, the most recent day on which our common stock was traded on the OTCQB, the closing price per share of our common stock as quoted on the OTCQB was $0.171.

As of September 30, 2019, the Company had 26,922,007 shares of common stock issued, par value $0.001, held by approximately 80 shareholders of record.

Dividend Policy

We have not paid any cash dividends on our common stock and do not plan to pay any such dividends in the foreseeable future. Our Board of Directors will determine our future dividend policy on the basis of many factors, including results of operations, capital requirements, and general business conditions.

Recent Sales of Unregistered Securities; Use of Proceeds from Registered Securities

There were no sales of unregistered securities during the fiscal year ended September 30, 2019.

ITEM 6. SELECTED FINANCIAL DATA

Not applicable to smaller reporting companies.

ITEM 7. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

The following discussion of our financial condition and results of operations should be read in conjunction with the consolidated financial statements and the notes to those financial statements that are included elsewhere in this annual report on Form 10-K.

FORWARD-LOOKING STATEMENTS

There are statements in this annual report on Form 10-K that are not historical facts. These “forward-looking statements” can be identified by use of terminology such as “believe”, “hope”, “may”, “anticipate”, “should”, “intend”, “plan”, “will”, “expect”, “estimate”, “project”, “positioned”, “strategy”, and similar expressions. You should be aware that these forward-looking statements are subject to risks and uncertainties that are beyond our control. For a discussion of these risks, you should read this entire annual report on Form 10-K document carefully. Although management believes that the assumptions underlying the forward-looking statements are reasonable, they do not guarantee our future performance, and actual results could differ from those contemplated by these forward-looking statements. The assumptions used for the purposes for the forward-looking statements specified in the following information represent estimates of future events and are subject to uncertainty as to possible changes in the economy, legislative changes, changes in the industry, and other circumstances. As a result, the identification and interpretation of data and other information and their use in developing and selecting assumptions from and among reasonable alternatives require the exercise of judgment. To the extent that the assumed events do not occur, the outcome may vary substantially from anticipated or projected results, and, accordingly, no opinion is expressed on the achievability of those forward-looking statements. In the light of these risks and uncertainties, there can be no assurance that the results and events contemplated by the forward-looking statements contained in this annual report on Form 10-K will in fact transpire. You are cautioned not to place reliance on these forward-looking statements, which speak only as of their dates. We do not undertake any obligation to update or revise any forward-looking statements.

| 9 |

OVERVIEW

Wall Street Media Co, Inc. (the “Company,” “we,” “us” or “our”) was organized as Mycatalogsonline.com, Inc. in the state of Nevada on January 6, 2009. In April 2009, the Company changed its name to My Catalogs Online, Inc. In August 2013, the Company changed its name to Wall Street Media Co., Inc.

The Company provides consulting and management services to entities looking to merge with, or acquire or otherwise consult with third party entities. These services are currently provided to Landmark-Pegasus, Inc., a related party (“Landmark-Pegasus”). Mr. Moroney also acts as Landmark-Pegasus’ President and is its sole director.

CRITICAL ACCOUNTING POLICIES

In response to the Securities and Exchange Commission’s (the “SEC”) financial reporting release, FR-60, Cautionary Advice Regarding Disclosure About Critical Accounting Policies, the Company has selected its more subjective accounting estimation processes for purposes of explaining the methodology used in calculating the estimate, in addition to the inherent uncertainties pertaining to the estimate and the possible effects on the Company’s financial condition. These accounting estimates are discussed below. These estimates involve certain assumptions that if incorrect could create a material adverse impact on the Company’s results of operations and financial condition

Revenue Recognition

As of October 1, 2018, the Company adopted Revenue from Contracts with Customers (Topic 606) (“ASC 606”). The new guidance sets forth a new five-step revenue recognition model which replaces the prior revenue recognition guidance in its entirety and is intended to eliminate numerous industry-specific pieces of revenue recognition guidance that have historically existed in U.S. GAAP. The underlying principle of the new standard is that a business or other organization will recognize revenue to depict the transfer of promised goods or services to customers in an amount that reflects what it expects to receive in exchange for the goods or services. The Company adopted the standard using the modified retrospective method and the adoption did not have a material impact on its financial statements.

The Company provides consulting service currently to a single client and represents the Company’s only revenue source. The Company recognizes revenue when the performance obligation (i.e. consulting services) with the customer are satisfied and when the service is provided. Revenue is measured as the amount of consideration the Company expects to receive in exchange for providing the service.

| 10 |

RESULTS OF OPERATIONS

FOR THE YEAR ENDED SEPTEMBER 30, 2019 COMPARED TO THE YEAR ENDED SEPTEMBER 30, 2018

Revenue: The Company’s revenues increased approximately 61% from $56,000 during the year ended September 30, 2018 to $90,290 for the year ended September 30, 2019 due to an increase in consulting services provided.

Operating Expenses: The Company’s operating expenses decreased approximately 12% from $70,752 during the year ended September 30, 2018 to $62,606 for the year ended September 30, 2019. The primary reason for this was due to a decrease in professional fees.

Interest Expense: The Company’s interest expense decreased approximately 3% from $4,522 during the year ended September 30, 2018 as compared to $4,370 for the year ended September 30, 2019 due to the repayments of notes payable during the year.

Income (Loss) from Operations: The Company’s income from operations increased approximately 288% from a loss from operations of $14,752 for the year ended September 30, 2018 as compared to income from operations of $27,684 for the year ended September 30, 2019. The primary reason for this was due to the increase in consulting services provided. $90,290 and $56,000, or 100%, of the Company’s revenue during the years ended September 30, 2019 and 2018, respectively, was derived from Landmark-Pegasus, a related party. Landmark-Pegasus is wholly owned by John Moroney, who beneficially owns approximately 59.8% of the Company’s common stock. Mr. Moroney also acts as Landmark-Pegasus’ President and is Landmark-Pegasus’ sole director.

LIQUIDITY AND CAPITAL RESOURCES

Net cash provided by operating activities was $26,853 for the year ended September 30, 2019 as compared to net cash used in operating activities of $7,748 for the year ended September 30, 2018.

Net cash used in financing activities was $23,290 for the year ended September 30, 2019 as compared to net cash provided by financing activities of $8,000 for the year ended September 30, 2018, primarily due to repayments of notes payable.

The working capital deficit was $95,361 for the year ended September 30, 2019 as compared to a working capital deficit of $118,675 for the year ended September 30, 2018.

As of September 30, 2019, the Company had approximately $8,375 in cash. The Company plans to fund ongoing operations by continuing to pursue contracts to provide consulting services in efforts to generate additional revenue. In addition, the Company is actively seeking investor funding.

RELATED PERSON TRANSACTIONS

For information on related party transactions and their financial impact, see Note 3 to the financial statements.

RECENTLY ISSUED ACCOUNTING PRONOUNCEMENTS

In February 2016, the FASB issued ASU 2016-02, “Leases” which, for operating leases, requires a lessee to recognize a right-of-use asset and a lease liability, initially measured at the present value of the lease payments, in its balance sheet. The standard also requires a lessee to recognize a single lease cost, calculated so that the cost of the lease is allocated over the lease term, on a generally straight-line basis. The ASU is effective for public companies for fiscal years beginning after December 15, 2018, including interim periods within those fiscal years. Early adoption is permitted. The Company has evaluated the impact of the adoption of ASU 2016-02 and does not currently believe that it will have a material impact on its financial statements and disclosures, since the company has no leases that are greater than one year.

OFF-BALANCE SHEET ARRANGEMENTS

We do not have any off-balance sheet arrangements that have or are reasonably likely to have a current or future effect on our financial condition, changes in financial condition, revenues or expenses, results of operations, liquidity, capital expenditures or capital resources, that is material to investors.

ITEM 7A. QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK

Not applicable for smaller reporting companies.

| 11 |

ITEM 8. FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA

INDEX TO FINANCIAL STATEMENTS

| 12 |

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

To the Board of Directors and

Stockholders of Wall Street Media Co., Inc.

Opinion on the Financial Statements

We have audited the accompanying balance sheets of Wall Street Media, Inc. (the Company) as of September 30, 2019, and the related statements of income, stockholders’ deficit and cash flows for the year ended September 30, 2019, and the related notes (collectively referred to as the financial statements). In our opinion, the financial statements present fairly, in all material respects, the financial position of the Company as of September 30, 2019 and the results of its operations and its cash flows for the year ended September 30, 2019, in conformity with accounting principles generally accepted in the United States of America.

Explanatory Paragraph- Going Concern

The accompanying financial statements have been prepared assuming that the Company will continue as a going concern. As discussed in Note 2 to the financial statements, the Company has suffered recurring losses. For the year ended September 30, 2019, the Company had a net income of $23,314 but had net cash used provided by operating activities of $26,853, accumulated deficit of $1,419,761 and negative working capital of $95,361. These factors raise substantial doubt about its ability to continue as a going concern. Management’s plans in regard to these matters are also described in Note 2. The financial statements do not include any adjustments that might result from the outcome of this uncertainty.

Basis for Opinion

These financial statements are the responsibility of the Company’s management. Our responsibility is to express an opinion on the Company’s financial statements based on our audits. We are a public accounting firm registered with the Public Company Accounting Oversight Board (United States) (PCAOB) and are required to be independent with respect to the Company in accordance with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our audit in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement, whether due to error or fraud. The Company is not required to have, nor were we engaged to perform, an audit of its internal control over financial reporting. As part of our audit, we are required to obtain an understanding of internal control over financial reporting, but not for the purpose of expressing an opinion on the effectiveness of the Company’s internal control over financial reporting. Accordingly, we express no such opinion.

Our audit included performing procedures to assess the risks of material misstatement of the financial statements, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence regarding the amounts and disclosures in the financial statements. Our audit also included evaluating the accounting principles used and significant estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that our audit provides a reasonable basis for our opinion.

| /s/ Assurance Dimensions | |

| We have served as the Company’s auditor since 2019. | |

| Coconut Creek, Florida | |

| November 1, 2019 |

| F-1 |

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

To the Board of Directors and

Stockholders of Wall Street Media Co, Inc.

Opinion on the Financial Statements

We have audited the accompanying balance sheet of Wall Street Media Co, Inc. (the Company) as of September 30, 2018, and the related statements of operations, changes in stockholders’ deficit, and cash flows for the year ended September 30, 2018, and the related notes (collectively referred to as the financial statements). In our opinion, the financial statements present fairly, in all material respects, the financial position of the Company as of September 30, 2018, and the results of its operations and its cash flows for the year ended September 30, 2018, in conformity with accounting principles generally accepted in the United States of America.

Going Concern

The accompanying financials have been prepared assuming the Company will continue as a going concern. As of September 30, 2018, the Company had accumulated losses of approximately $1,443,000, has generated limited profit, and may experiences losses in the near term. These factors and the need for additional financing in order for the Company to meet its business plan, raise substantial doubt about its ability to continue as a going concern. Management’s plan to continue as a going concern is also described in Note 2. The financial statements do not include any adjustments that might result from the outcome of this uncertainty.

Basis for Opinion

These financial statements are the responsibility of the Company’s management. Our responsibility is to express an opinion on the Company’s financial statements based on our audit. We are a public accounting firm registered with the Public Company Accounting Oversight Board (United States) (PCAOB) and are required to be independent with respect to the Company in accordance with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our audit in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement, whether due to error or fraud. The Company is not required to have, nor were we engaged to perform, an audit of its internal control over financial reporting. As part of our audit, we are required to obtain an understanding of internal control over financial reporting, but not for the purpose of expressing an opinion on the effectiveness of the Company’s internal control over financial reporting. Accordingly, we express no such opinion.

Our audit included performing procedures to assess the risks of material misstatement of the financial statements, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence regarding the amounts and disclosures in the financial statements. Our audit also included evaluating the accounting principles used and significant estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that our audit provides a reasonable basis for our opinion.

|

|

| Soles, Heyn & Company, LLP | |

| We have served as the Company’s auditor since 2018. | |

| West Palm Beach, Florida | |

| December 27, 2018 |

| F-2 |

Balance Sheets

| September 30, 2019 | September 30, 2018 | |||||||

| ASSETS | ||||||||

| Current Assets | ||||||||

| Cash | $ | 8,375 | $ | 4,812 | ||||

| Accounts receivable-related party | - | 2,500 | ||||||

| Total Current Assets | 8,375 | 7,312 | ||||||

| Deposits | 578 | 578 | ||||||

| Total Assets | $ | 8,953 | $ | 7,890 | ||||

| LIABILITIES AND STOCKHOLDERS’ DEFICIT | ||||||||

| Current Liabilities | ||||||||

| Accounts payable and accrued expenses | $ | - | $ | 3,331 | ||||

| Accrued interest payable | 13,736 | 9,366 | ||||||

| Notes payable -related parties | 90,000 | 113,290 | ||||||

| Total current liabilities | 103,736 | 125,987 | ||||||

| Total Liabilities | 103,736 | 125,987 | ||||||

| Commitments and Contingencies (Note 6) | ||||||||

| Stockholders’ Deficit | ||||||||

| Preferred stock, $0.001 par value; 5,000,000 shares authorized; none issued or outstanding | - | - | ||||||

| Common stock, $0.001 par value; 195,000,000 shares authorized; 26,922,007 issued and outstanding at September 30, 2019 and 2018 | 26,922 | 26,922 | ||||||

| Additional paid-in capital | 1,298,056 | 1,298,056 | ||||||

| Accumulated deficit | (1,419,761 | ) | (1,443,075 | ) | ||||

| Total stockholders’ deficit | (94,783 | ) | (118,097 | ) | ||||

| Total Liabilities and Stockholders’ Deficit | $ | 8,953 | $ | 7,890 | ||||

The accompanying notes are an integral part of these financial statements.

| F-3 |

Statements of Operations

| For the year ended | For the year ended | |||||||

| September 30, 2019 | September 30, 2018 | |||||||

| Revenues: | ||||||||

| Consulting fees from related party | $ | 90,290 | $ | 56,000 | ||||

| Total Revenues | 90,290 | 56,000 | ||||||

| Operating Expenses: | ||||||||

| Programming and development | 620 | 1,445 | ||||||

| Office and administrative | 16,753 | 16,699 | ||||||

| Professional fees | 43,733 | 49,427 | ||||||

| Rent | 1,500 | 3,181 | ||||||

| Total Operating Expenses | 62,606 | 70,752 | ||||||

| Income (Loss) From Operations | 27,684 | (14,752 | ) | |||||

| Other (Expense) | ||||||||

| Interest expense | (4,370 | ) | (4,522 | ) | ||||

| Total Other (Expense) Income | (4,370 | ) | (4,522 | ) | ||||

| Net income (loss) | $ | 23,314 | $ | (19,274 | ) | |||

| Net income (loss) per share - basic | $ | 0.00 | $ | (0.00 | ) | |||

| Net income(loss) per share - diluted | $ | 0.00 | $ | (0.00 | ) | |||

| Weighted average number of common shares - Basic and Diluted | 26,922,007 | 26,922,007 | ||||||

The accompanying notes are an integral part of these financial statements.

| F-4 |

Statements of Changes in Stockholders’ Deficit

For the Years ended September 30, 2019 and 2018

| Additional | Total | |||||||||||||||||||

| Common Stock | Paid-in | Accumulated | Stockholders’ | |||||||||||||||||

| Shares Issued | Amount | Capital | Deficit | Deficit | ||||||||||||||||

| Balance at September 30, 2017 | 26,922,007 | $ | 26,922 | $ | 1 ,298,056 | $ | (1,423,801 | ) | $ | (98,823 | ) | |||||||||

| Net loss | - | - | - | (19,274 | ) | (19,274 | ) | |||||||||||||

| Balance at September 30, 2018 | 26,922,007 | 26,922 | 1,298,056 | (1,443,075 | ) | (118,097 | ) | |||||||||||||

| Net income | - | - | - | 23,314 | 23,314 | |||||||||||||||

| Balance at September 30, 2019 | 26,922,007 | $ | 26,922 | $ | 1,298,056 | $ | (1,419,761 | ) | $ | (94,783 | ) | |||||||||

The accompanying notes are an integral part of these financial statements.

| F-5 |

Statements of Cash Flows

| For the year ended | For the year ended | |||||||

| September 30, 2019 | September 30, 2018 | |||||||

| Cash flows provided by (used in) Operating Activities: | ||||||||

| Net income (loss) | $ | 23,314 | $ | (19,274 | ) | |||

| Changes in operating assets and liabilities: | ||||||||

| Accounts receivable | 2,500 | 7,500 | ||||||

| Accrued expenses | (3,331 | ) | (496 | ) | ||||

| Accrued interest payable | 4,370 | 4,522 | ||||||

| Net cash provided by (used in) operating activities | 26,853 | (7,748 | ) | |||||

| Cash flows (used in) provided by Financing Activities: | ||||||||

| Repayments of notes payable-related parties | (23,290 | ) | - | |||||

| Proceeds from issuance of notes payable-related parties | - | 8,000 | ||||||

| Net cash (used in) provided by financing activities | (23,290 | ) | 8,000 | |||||

| Increase in cash during the year | 3,563 | 252 | ||||||

| Cash, beginning of year | 4,812 | 4,560 | ||||||

| Cash, end of year | $ | 8,375 | $ | 4,812 | ||||

| SUPPLEMENTAL DISCLOSURE OF CASH FLOW INFORMATION | ||||||||

| Interest paid in cash | $ | - | $ | - | ||||

| Taxes paid in cash | $ | - | $ | - | ||||

The accompanying notes are an integral part of these financial statements.

| F-6 |

Notes to Financial Statements

For the Years Ended September 30, 2019 and 2018

Note 1 - Nature of Operations and Summary of Significant Accounting Policies

Nature of Operations

Wall Street Media Co, Inc. (the “Company” or “Wall Street Media”) was organized as Mycatalogsonline.com, Inc. in the state of Nevada on January 26, 2009. In April 2009, the Company changed its name to My Catalogs Online, Inc. In August 2013 the Company changed its name to Wall Street Media Co, Inc.

The Company provides consulting and management services to entities looking to merge with or acquire or otherwise consult with third party entities. These services are currently provided to Landmark-Pegasus, Inc., a related party (“Landmark-Pegasus”). Landmark-Pegasus is owned by John Moroney, the Company’s majority shareholder. Mr. Moroney also acts as Landmark-Pegasus’ President.

Use of Estimates

The financial statements are prepared in accordance with Accounting Principles Generally Accepted in the United States (“GAAP”). These accounting principles require the Company to make certain estimates, judgments and assumptions. The Company believes that the estimates, judgments and assumptions upon which it relies are reasonable based upon information available at the time that these estimates, judgments and assumptions are made. These estimates, judgments and assumptions can affect the reported amounts of assets and liabilities as of the date of the financial statements as well as the reported amounts of revenues and expenses during the periods presented. The financial statements would be affected to the extent there are material differences between these estimates and actual results. In many cases, the accounting treatment of a particular transaction is specifically dictated by GAAP and does not require management’s judgment in its application. There are also areas in which management’s judgment in selecting any available alternative would not produce a materially different result. Significant estimates include the valuation allowance on deferred tax assets.

Revenue Recognition

As of October 1, 2018, the Company adopted Revenue from Contracts with Customers (Topic 606) (“ASC 606”). The new guidance sets forth a new five-step revenue recognition model which replaces the prior revenue recognition guidance in its entirety and is intended to eliminate numerous industry-specific pieces of revenue recognition guidance that have historically existed in U.S. GAAP. The underlying principle of the new standard is that a business or other organization will recognize revenue to depict the transfer of promised goods or services to customers in an amount that reflects what it expects to receive in exchange for the goods or services. The Company adopted the standard using the modified retrospective method and the adoption did not have a material impact on its financial statements.

The Company provides consulting service currently to a single client and represents the Company’s only revenue source. The Company recognizes revenue when the performance obligation (i.e. consulting services) with the customers are satisfied and when the service is provided. Revenue is measured as the amount of consideration the Company expects to receive in exchange for providing the service.

| F-7 |

Wall Street Media Co., Inc.

Notes to Financial Statements

For the Years Ended September 30, 2019 and 2018

Reclassification

Certain amounts in prior periods have been reclassified to conform to the current year presentation. This includes the reclassification of revenue consulting fees -other to consulting fees - related party, and income taxes for net operating losses carried forward.

Accounts Receivable

Accounts receivable arise from the normal course of business and is considered collectible within one year. Any allowance for doubtful accounts would be based on historical trends and approved by management. There were no accounts receivable nor an allowance for doubtful accounts at September 30, 2019.

Income Taxes

The Company accounts for income taxes pursuant to the provisions of ASC 740-10 “Accounting for Income Taxes,” which requires, among other things, an asset and liability approach to calculating deferred income taxes. The asset and liability approach requires the recognition of deferred tax assets and liabilities for the expected future tax consequences of temporary differences between the carrying amounts and the tax bases of assets and liabilities. A valuation allowance is provided to offset any net deferred tax assets for which management believes it is more likely than not that the net deferred asset will not be realized.

Upon inception, the Company adopted the provisions of ASC 740-10, Accounting for Uncertain Income Tax Positions. In accordance with the guidance of ASC 740-10, the benefit of a tax position is recognized in the financial statements in the period during which, based on all available evidence, management believes it is more likely than not that the position will be sustained upon examination, including the resolution of appeals or litigation processes, if any. Tax positions taken are not offset or aggregated with other positions. Tax positions that meet the more-likely-than-not recognition threshold are measured as the largest amount of tax benefit that is more than 50 percent likely of being realized upon settlement with the applicable taxing authority. The portion of the benefits associated with tax positions taken that exceeds the amount measured as described above should be reflected as a liability for unrecognized tax benefits in the accompanying balance sheet along with any associated interest and penalties that would be payable to the taxing authorities upon examination. The Company believes its tax positions are all highly certain of being upheld upon examination. As such, the Company has not recorded a liability for unrecognized tax benefits. As of September 30, 2019, tax years 2019, 2018, 2017, and 2016 remain open for Internal Revenue Service audit. The Company has received no notice of audit from the Internal Revenue Service for any of the open tax years.

Basic and Diluted Net Loss per Common Share

Basic net loss per share is computed by dividing the net loss by the weighted average number of common shares outstanding during the period. Diluted net loss per common share is computed by dividing the net loss by the weighted average number of common shares outstanding for the period and, if dilutive, potential common shares outstanding during the period. Potentially dilutive securities consist of the incremental common shares issuable upon exercise of common stock equivalents such as stock options and convertible debt instruments. Potentially dilutive securities are excluded from the computation if their effect is anti-dilutive. There were no potentially dilutive securities outstanding as of September 30, 2019 and 2018.

| F-8 |

Wall Street Media Co., Inc.

Notes to Financial Statements

For the Years Ended September 30, 2019 and 2018

Recent Accounting Pronouncements

In February 2016, the FASB issued ASU 2016-02, “Leases” which, for operating leases, requires a lessee to recognize a right-of-use asset and a lease liability, initially measured at the present value of the lease payments, in its balance sheet. The standard also requires a lessee to recognize a single lease cost, calculated so that the cost of the lease is allocated over the lease term, on a generally straight-line basis. The ASU is effective for public companies for fiscal years beginning after December 15, 2018, including interim periods within those fiscal years. Early adoption is permitted. This ASU is effective for us on October 1, 2019. The Company has evaluated the impact of the adoption of ASU 2016-02 and does not currently believe that it will have a material impact on its financial statements and disclosures since it does not have any lease which meets the criteria.

Note 2 - Going Concern

As reflected in the accompanying financial statements for the years ended September 30, 2019 and 2018, the Company reported a net income of $23,314 and net loss of $19,274, respectively, and net cash provided by operating activities of $26,853 in 2019 and net cash used in operating activities of $7,748 in 2018. In addition, the Company has a working capital deficit of $95,361 at September 30, 2019. These matters raise substantial doubt about the Company’s ability to continue as a going concern. The financial statements do not include any adjustments relating to the recovery of the recorded assets or the classification of the liabilities that might be necessary should the Company be unable to implement its business plan and continue as a going concern. In addition, the Company is actively seeking investor funding.

Note 3 – Related Party Transactions

$90,290 and $56,000, or 100% of the Company’s revenue during the years ended September 30, 2019 and 2018, respectively, was derived from Landmark-Pegasus, a related party. Landmark-Pegasus is wholly owned by John Moroney, who beneficially owns approximately 59.8% of the Company’s common stock. Mr. Moroney also acts as Landmark-Pegasus’ President and is Landmark-Pegasus’ sole director.

In November 2014, January 2015, April 2015 and August 2015, the Company received $20,000, $20,000, $10,000 and $10,000 respectively, from the issuance of notes payable to Landmark-Pegasus that accrue interest at an annual rate of 4%, and are payable on demand. During the fiscal years ended September 30, 2016 and 2017, the Company received an additional $28,890 and $11,500, respectively, payable to Landmark-Pegasus on demand at an interest rate of 4% annually. During the fiscal year ended September 30, 2018, the Company received an additional $8,000. During 2019 the Company made $23,290 in repayments, decreasing the balance on the notes to $90,000 as of September 30, 2019 payable to Landmark-Pegasus on demand at an interest rate of 4% annually.

Jeffrey A. Lubchansky, the Company’s Chairman of the Board, President, Chief Executive Officer and principal financial officer, received $12,000 during the year ended September 30, 2019 as compensation for his services as an executive officer. His compensation is $1,000 per month plus out-of-pocket expenses. This amount is included in Professional fees on the Statement of Operations.

Note 4 – Stockholders’ Deficit

The Company has 5,000,000 preferred shares authorized. None are designated, issued or outstanding. The Company has 195 million common stock authorized and has 26,922,007 shares issued and outstanding at September 30, 2019 and 2018.

| F-9 |

Wall Street Media Co., Inc.

Notes to Financial Statements

For the Years Ended September 30, 2019 and 2018

Note 5 – Income Taxes

There was no income tax expense in fiscal 2019 and 2018 due to the Company’s net taxable losses.

The reconciliation of income tax expense (benefit) for the years ended September 30, 2019 and 2018 computed at the United States federal tax rate of 21% to income tax expense (benefit) is as follows:

| 2019 | 2018 | |||||||

| Tax expense (benefit) at the United States statutory rate | $ | 4,686 | $ | (4,048 | ) | |||

| State income tax, net of federal | 1,058 | (914 | ) | |||||

| Change in tax rate and 382 limitation | - | 78,911 | ||||||

| Change in valuation allowance | (5,744 | ) | (73,949 | ) | ||||

| Income tax expense (benefits) | $ | - | $ | - | ||||

| Tax expense (benefit) at the United States statutory rate | 21.00 | % | (24.53 | )% | ||||

| State income tax, net of federal | 4.74 | % | (4.53 | )% | ||||

| Change in tax rate and 382 limitation | - | 412.73 | % | |||||

| Change in valuation allowance | (25.74 | )% | (383.67 | )% | ||||

| Income tax expense (benefits) | - | - | ||||||

The tax effect of temporary differences that give rise to significant portions of the deferred tax assets is as follows:

| 2019 | 2018 | |||||||

| Net operating loss carryforward | $ | 41,046 | $ | 46,789 | ||||

| Valuation allowance | (41,046 | ) | (46,789 | ) | ||||

| Net deferred tax assets | $ | - | $ | - | ||||

Deferred income taxes reflect the net tax effects of temporary differences between the carrying amounts of assets and liabilities for financial reporting purposes and the amounts used for income tax purposes. At September 30, 2019, the Company has net operating losses (“NOL”) of approximately $656,000 that will expire from 2031 to 2038. Under IRS Code Section 382, the annual allowable NOL deduction will be limited to $31,000 per year for years 2011-2015 due to a change in control that occurred in 2015.

A valuation allowance is established if it is more likely than not that all or a portion of the deferred tax asset will not be realized. Accordingly, a valuation allowance was established at September 30, 2019 and 2018 for the full amount of our deferred tax assets due to the uncertainty of realization. Management believes that based upon its projection of future taxable operating income for the foreseeable future, it is more likely than not that the Company will not be able to realize the benefit of the deferred tax assets at September 30, 2019 and 2018.

Note 6 – Commitments and Contingencies

From time to time, we may be involved in litigation relating to claims arising out of our operations in the normal course of business. As of September 30, 2019 and 2018, there were no pending or threatened lawsuits that could reasonably be expected to have a material effect on our results of operations.

Note 7 – Concentrations

During the fiscal years ended September 30, 2019 and 2018, 100%, respectively, of the Company’s revenue was derived from Landmark-Pegasus, a related party. Landmark-Pegasus is wholly owned by John Moroney, who beneficially owns approximately 59.8% of the Company’s common stock. Mr. Moroney also acts as Landmark-Pegasus’ President and is Landmark-Pegasus’ sole director.

| F-10 |

ITEM 9. CHANGES AND DISAGREEMENTS WITH ACCOUNTANTS ON ACCOUNTING AND FINANCIAL DISCLOSURE

None.

ITEM 9A. CONTROLS AND PROCEDURES

Evaluation of Disclosure Controls and Procedures

We carried out an evaluation required by Rule 13a-15(b) of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), under the supervision and with the participation of our management, including our Chief Executive Officer and principal financial officer, of the effectiveness of the design and operation of our disclosure controls and procedures, as such term is defined in Exchange Act Rule 13a–15(e). Disclosure controls and procedures are designed with the objective of ensuring that (i) information required to be disclosed in an issuer’s reports filed under the Exchange Act is recorded, processed, summarized and reported within the time periods specified in the SEC rules and forms and (ii) information is accumulated and communicated to management, including our Chief Executive Officer and principal financial officer, as appropriate to allow timely decisions regarding required disclosures.

The evaluation of our disclosure controls and procedures included a review of our objectives and processes and effect on the information generated for use in this report. This type of evaluation is done quarterly so that the conclusions concerning the effectiveness of these controls can be reported in our periodic reports filed with the SEC. We intend to maintain these controls as processes that may be appropriately modified as circumstances warrant.

Based on their evaluation, our Chief Executive Officer and principal financial officer has concluded that our disclosure controls and procedures are not effective in timely alerting our Chief Executive Officer and principal financial officer to material information which is required to be included in our periodic reports filed with the SEC as of the end of the period covering this annual report on Form 10-K.

Management’s Annual Report on Internal Control Over Financial Reporting

Our management is responsible for establishing and maintaining adequate internal control over financial reporting, as such term is defined in Exchange Act Rule 13a-15(f). Under the supervision and with the participation of our management, including our Chief Executive Officer and principal financial officer, we conducted an evaluation of the effectiveness of our internal control over financial reporting as of September 30, 2019, based on the criteria set forth in Internal Control — Integrated Framework issued by the Committee of Sponsoring Organizations of the Treadway Commission (2013). Based on this evaluation, our management concluded that our internal control over financial reporting was not effective as of September 30, 2019.

A control system, no matter how well conceived and operated, can provide only reasonable, not absolute, assurance that the objectives of the control system are met. Management necessarily applied its judgment in assessing the benefits of controls relative to their costs. Because of the inherent limitations in all control systems, no evaluation of controls can provide absolute assurance that all control issues and instances of fraud, if any, within the Company have been detected. The design of any system of controls is based in part upon certain assumptions about the likelihood of future events, and there can be no assurance that any design will succeed in achieving its stated goals under all potential future conditions, regardless of how remote. Because of the inherent limitations in a control system, misstatements due to error or fraud may occur and may not be detected.

This annual report on Form 10-K does not include an attestation report of our independent registered public accounting firm regarding the Company’s internal control over financial reporting. We were not required to have, nor have we engaged our independent registered public accounting firm to perform, an audit on our internal control over financial reporting pursuant to the rules of the SEC that permit us to provide only management’s report in this annual report on Form 10-K.

Changes in Internal Control Over Financial Reporting

During our most recent fiscal quarter, there has not been any change in our internal control over financial reporting as such term is defined in Exchange Act Rule 13a-15(f) that has materially affected, or is reasonably likely to affect, our internal control over financial reporting.

None.

| 13 |

ITEM 10. DIRECTORS, EXECUTIVE OFFICERS AND CORPORATE GOVERNANCE

The following table sets forth the name, position and age of our sole director and executive officer as of the date of this annual report on Form 10-K. Our directors are elected by our stockholders at each annual meeting and serve for one year and until their successors are elected and qualified. Officers are elected by our board of directors and their terms of office are at the discretion of our board.

| Name | Age | Position | ||

| Jeffrey A. Lubchansky | 66 | Chairman of the Board, Director, President and Chief Executive Officer |

Biographical information concerning our director and executive officer listed above is set forth below.

Jeffrey A. Lubchansky. Mr. Lubchansky has served as the Company’s President, Chief Executive Officer and Chairman of the Board since October 2015. He is a Certified Public Accountant who has been at the forefront of integrating technology into the accounting field and providing leadership in management, taxation and accounting in various industries. These industries include sports/entertainment, real estate, financial institutions, highly compensated individuals, nutraceuticals, health and beauty, medical devices, audio/visual and consulting and tax services to CPA firms and attorneys.